In a functioning market, financial speculation exclusively serves the demand for risk hedging of market players.

Photo: adobestock.com/ Gorodenkoff

Download this article in magazine layout

Download this article in magazine layout

- Share this article

- Subscribe to our newsletter

Food price inflation, its causes and speculation risks

The world economy is currently facing significant challenges: high inflation, food and energy insecurity, elevated debt levels, tightened financial conditions, volatility in capital flows and exchange rates, and the intensification of geopolitical tensions. The sharp and persistent rise in inflation, which started in 2021 and grew to distressing dimensions in 2022, is causing concern, above all for the world’s poor, and is expected to increase food insecurity world-wide. The impact of inflation is not felt equally across economies. Low- and middle-income countries tend to be more vulnerable to high inflation than developed, richer countries, as lowest-income households in emerging and developing economies spend roughly 50 per cent of their income on food, while the highest-income households spend only 20 per cent. While higher food prices could benefit food sellers in developing economies, most of the poor are net buyers of food, so food-price spikes tend to have acute impacts on human health and living standards, increasing overall poverty and amplifying the risks of social unrest and political instability. In 2022, 828 million people were suffering from undernourishment, a 150 million increase from 2019, about 260 million were in acute hunger, and more than 3 billion people could not afford a healthy diet.

Food price inflation causes – supply constraints and macro-economic factors

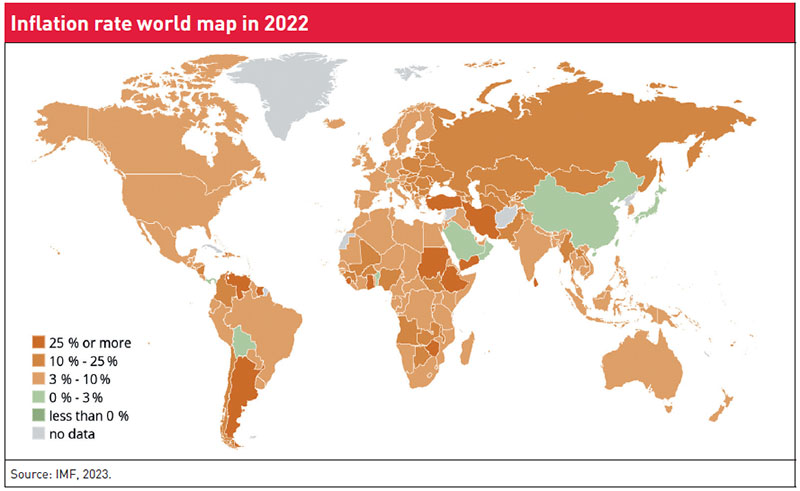

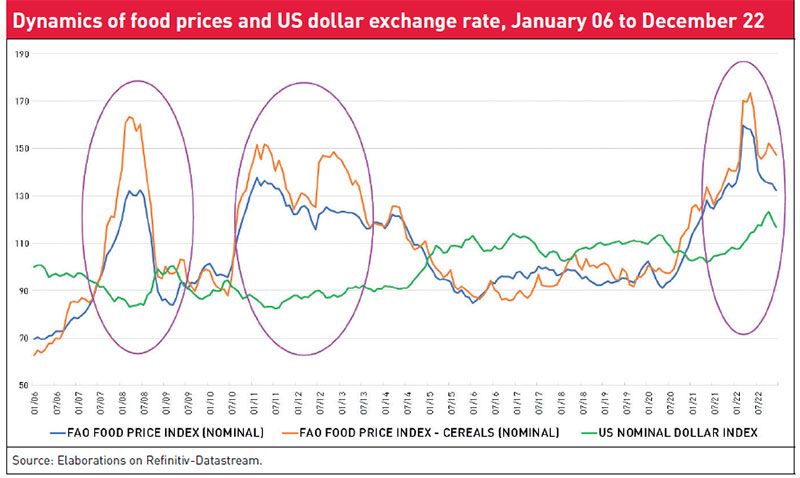

The FAO Food Price Index climbed by 50 per cent between the end of 2020 and March 2022. This was driven by price increases for wheat (100 %), for rice (25 %), and for maize (100 %) at some point in 2021 as compared to pre-Covid levels. During the same period, prices of oil, natural gas and chemical fertilisers started to rise. In early March 2022, during the first days of the Russian invasion in Ukraine, wheat and maize prices jumped by close to 50 per cent within just a few days. Rising international food and energy prices have increased inflationary pressure all around the world. While international grain prices returned to pre-war levels in the second half of 2022, inflation world-wide remains strikingly high. Whereas in October 2021, only 20 out of 146 countries in the world registered inflation rates above 10 per cent, by October 2022, this number had more than tripled, with 68 out of 146 countries (most of which are developing economies) registering inflation rates above 10 per cent (see Figure).

The reasons for the steep rise in food inflation in 2021 and 2022 are multifaceted and result from a confluence of different inflationary forces and multiple shocks, reflecting marked supply chain and logistical disruptions due to the pandemic first and the Russian-Ukrainian war later, the rising global demand following the partial world-wide economic recovery in 2021, elevated inflation expectations, the eroding value of national currencies against the US dollar and speculative trading in commodities. Since February 2022, the war in Ukraine has amplified pre-existing stresses in the global commodity markets, shoving prices up. The cost of oil and gas rose by a third as Western countries imposed sanctions on Russia, a major producer and exporter of both commodities and fertiliser (together with its sanctioned ally Belarus). Food prices also reached historic heights, pushed up by input and transportation costs, as well as by Russia’s blockades of grain exports from Ukraine, the fifth-largest exporter of wheat (Russia was until recently the first world exporter). Together they accounted (pre-war) for twelve per cent of all calories traded globally. In 2021-2022, then, a series of extreme climatic events reduced the production of some agricultural products. For example, Brazil experienced the worst drought in a century and, in July 2022, the worst frost in 20 years, both of which harmed several crops. Four-season drought has hit Ethiopia and Kenya. Lack of rain and extreme temperatures in India, along America’s wheat belt and in the Beauce region of France also enlarged world-wide concerns. This was accompanied by uncertainties about trade policy restrictions.

On top of food price inflation, mainly linked to tight supply-demand conditions and eroding value of national currencies, inflationary pressures of 2021-2022 were driven by a combination of factors, including different policy stimuli (the generous pandemic-relief fiscal measures and expansive monetary policies) in each country. These factors impacted inflation dynamics in varying proportions. For example, inflation in sub-Saharan Africa and other African countries was mainly pushed by elevated global food prices, especially wheat, maize, rice, and sorghum and energy prices accompanied by national depreciations. Egypt, for instance, imports 86 per cent of its whole wheat and 26 per cent of its maize from Russia and Ukraine, and the Egyptian pound went down by 18 per cent. Except for Ethiopia and Ghana, where the excess in domestic demand arising from expansionary fiscal policies has contributed to price pressure, in all African countries, the major drivers of inflation have been external factors (global commodity prices and supply chain disruptions, i.e. imported inflation). In Latin America, price pressures became stronger because of expansive monetary policies as a consequence of the pandemic response, wage indexation and, in some cases, strong aggregate demand. In Chile, pandemic-related financial support, together with pension withdrawals, heightened consumer spending significantly, fuelling inflation, whereas in Colombia, inflation surged mainly because of higher oil and commodity prices. In Asia, food price increases during the Covid-19 pandemic were slightly higher than in Africa, averaging about 50 per cent for some products compared to 2019, while most East Asian countries were generally less vulnerable to food price inflation in 2022, thanks to stable rice prices. Syria, Lebanon, Afghanistan and Yemen (partly Indonesia and the Philippines as well) also experienced extreme food price spikes.

How is this crisis different from the food crisis 2008–2012?

The post-2020 price development and the 2022 price spike show some similarities to the 2008-2012 price spikes. However, there are also some differences between the 2008-2012 crisis and the current food and inflation crisis. In particular, the 2008-2012 crisis was mainly a food crisis, and inflation was not further triggered by monetary and fiscal policies. The impact of energy prices (oil and fertilisers) has been more pronounced in the recent spike, also because input markets have become more integrated. Instead, international macroeconomic factors, such as the role of the exchange rate and growing demand from emerging economies, are less pronounced than in 2008–2012.

The 2008–2012 food crisis emerged from poor harvests at the beginning of 2008 and supply shortages because of low grain stocks. International linkages in the global food system were only developing during the 2000s, and were much lower than today. Therefore, the impact of international shocks on domestic food systems was unexpectedly strong. Post-2020 food systems are more strongly interlinked. This involves global food supply chains in input and output markets. Therefore, international food price pass-through to domestic food markets is faster and stronger. Moreover, economic slowdowns as a result of the Covid-19 pandemic hit low- and middle-income countries much more than the international financial crisis which started in mid-2007. Stimulus spending and expansive monetary policies have contributed to inflation on top of the international component. In consequence, the reduction in global food prices reduces inflationary pressure, but will not automatically lead to lower overall inflation.

The role of speculation

Given seasonal production and climate-related fluctuations in yields, speculative storage of grains and oilseeds has been applied for thousands of years and contributes to offsetting supply shocks. Today, financial speculation – trading at commodity futures markets – plays an important role in stabilising agricultural commodity prices and reducing the risk for consumers and producers (see Box below). The overall share of grain and oilseed produce that goes through formalised commodity markets has steadily increased over the last decades, and today, price developments at commodity exchanges strongly influence spot markets around the world. In a functioning market, financial speculation exclusively serves the demand for risk hedging of market players. Prices are determined by fundamentals, i.e. the long-term, basic information about real production possibilities and the structures of the market. When speculative activity becomes rampant and financial speculators trade mainly among themselves, financial speculation gets excessive, and prices may deviate from supply or demand expectations in the market.

Commodity futures markets for staple foods – benefits and risks

Commodity futures markets have three important economic functions. First, they help producers, traders, and processors (commercial market actors or hedgers) hedge their price risks; i.e. they take price risks from less risk-averse hedgers. Second, they are important for price discovery in spot markets by enabling commodity traders to establish benchmarks for current prices. Finally, derivatives markets provide transaction efficiency by reducing transaction costs. As a result, investments become more productive and price volatility decreases. For these reasons, speculation is a necessary part of financial markets, and it is counterproductive to completely exclude food commodities from speculative transactions.

Financial speculation comprises buying, holding, selling and short-selling of commodities to profit from price fluctuations. Speculative trading without an interest in the use of the commodity is referred to as non-commercial trading/ financial speculation. Excessive speculation can cause price shocks in commodity futures markets and jeopardise financial market stability once speculators' behaviour is driven by financial market strategies rather than market fundamentals. Following the stock market crash in 2002, agricultural commodities became a popular asset class in the portfolios of financial institutions and the general investment community because of their relatively low correlation with returns of other asset classes. During this period, trading in agricultural commodity futures and options contracts increased sharply. As a result, speculative activity also rose dramatically. Critics therefore hold speculation partly responsible for the commodity price boom in the 2000s.

The assessment of the role of financial speculation in the 2021-2022 food price developments should not be viewed in isolation, because commodity trading is also related to the market development in other asset classes, such as equities, government bonds, and even real estate. A valid valuation can usually only be carried out in the aftermath of a crisis. However, the sudden price hike in March 2022 when wheat prices increased by 52 per cent at the Chicago Mercantile Exchange (CME) and by 39 per cent at the Euronext Exchange in Paris was been a very exceptional case. At this time, representing a trend starting at the end of 2020, investments of financial speculators, like hedge funds, in agricultural commodities were very high. These speculators were betting on rising commodity futures prices, a behaviour that corresponded with price spikes in commodity futures markets in 2007–2008.

The Excessive Food Price Variability Early Warning System maintained by the International Food Policy Research Institute (IFPRI) also reported abnormal market dynamics between the third quarter of 2021 and the second quarter of 2022 which could have led to excessive financial speculation. Yet this does not necessarily indicate that the increased financial market speculation contributed to the price hike in early 2022 because it also highlights an increased need of producers or sellers to hedge against the risk of falling prices. Since the second half of 2022, futures and spot prices of agricultural commodities have fallen to pre-war levels. At the same time, the investments of financial speculators in commodity markets have also significantly declined. This trend corresponds to significant reductions in market uncertainties in 2022. For instance, over-land grain transports and the Black Sea Grain Initiative in June 2022 ensured that Ukraine grain exports have been available to the world market. While it will require further analysis to assess whether and to what extent excessive speculation contributed to the price increases in cereals in the first half of 2022, a re-rise in agricultural commodity prices cannot be ruled out given the prolonged uncertainties of Russian and Ukraine export levels.

What measures have to be taken by politics to counter food price inflation and volatility?

The current situation requires immediate policy responses as well as long-term changes and a transformation of the global food system.

Immediate responses include:

- Improving the short-run functioning of the global food market through political coordination at the G20 and UN levels (i.e. keep food and fertiliser markets open to avoid the direct or indirect impact of economic sanctions on the food security of third countries).

- Strengthening the Rome-based food agencies, the World Trade Organization (WTO) and AMIS (see page 13) to increase market transparency, trade functioning and policy coordination.

- Improving the coordination of fiscal and monetary policies to bring inflation down, while maintaining safety policies.

- Increasing debt relief, food aid and budget support to expand social protection, including scaling humanitarian efforts in and around hunger-prone zones impacted by climate crises and conflicts.

Long-term responses include:

- Strengthening sustainable productivity growth and sustainable land use, especially in low-income countries, with technologies and innovations to enhance crises resilience.

- Improving the efficiency of fertiliser usage by increasing fertiliser availability in Africa through local production and trade, increasing nutrient efficiency world-wide and the expansion of sustainable soil and land use. The latter is called for from a climate policy perspective in any case.

- Restructuring the global food system (without counteracting environmental and climate goals) by disincentivising the demand for bioenergy based in field crops and meat in high-income countries to expand food production and availability.

- Building and supporting strong macro-fiscal institutions, e.g. an import facilitation mechanism, to buffer commodity price volatility.

- Redesigning the ongoing follow-up to the UN Food Systems Summit 2021 to add global food crises response and global food systems reform issues to the UN agenda, in addition to national pathways of food systems transformations.

Bernardina Algieri is Associate Professor in Economics at Italy’s University of Calabria, Department of Economics, Statistics and Finance. Her research areas include commodity markets, food prices, international trade, and applied and development economics.

Lukas Kornher is a Senior Researcher at the Center for Development Research (ZEF) at the University of Bonn, Germany, where he coordinates research on markets and trade and impacts on food and nutrition security. His research focuses on global and local food markets, price formation and the role of trade.

Joachim von Braun is a Distinguished Professor of Economics and Technical Change at Bonn University’s Center for Development Research and President of the Pontifical Academy of Sciences. His main areas of expertise include research on development economics and policy, food security, nutrition and health, agricultural economics, natural resources, poverty and science policy.

Contact: lkornher(at)uni-bonn.de

News Comments

Current Print Issue

Add a comment

Be the First to Comment