The value of global trade in agricultural commodities has increased fourfold over the past 20 years.

Photo: Pradeep Gaurs/ shutterstock.com

Agrifood prices and international trade flows

International trade facilitates the movement of food from surplus to deficit regions, helping to alleviate food shortages and stabilise prices. However, high trade dependence makes a country's food supply vulnerable to trade disruptions, as seen recently during the Covid-19 crisis and the Ukraine-Russia conflict. Global trade in agricultural commodities is an important aspect of agricultural production and consumption and is growing, with the value of trade flows increasing fourfold over the past 20 years.

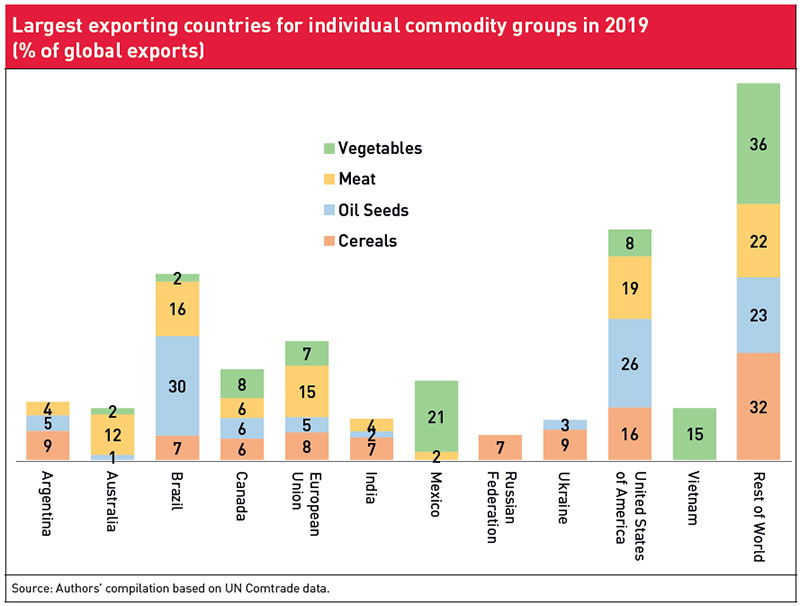

The most traded commodity groups by value are fruits and vegetables (23 %), cereals (14 %), fish and meat (11 % each) and oilseeds (8%). At product level, the most traded product by value is the oil seed soy, followed by cereals wheat and maize. China is the world's largest importer of soy. The country's large population, growing demand for meat products and expanding livestock industry have led to a significant increase in soy imports. The largest bilateral trade flows for any single commodity is soy from Brazil and the USA to China. Chinese meat imports from Latin America and Europe are also considerable. Agricultural trade is highly concentrated. While there is some variation between commodity groups, the large majority of global agricultural trade is accounted for by just 11 countries. Trade shares by commodity group and region are depicted in the Figure below.

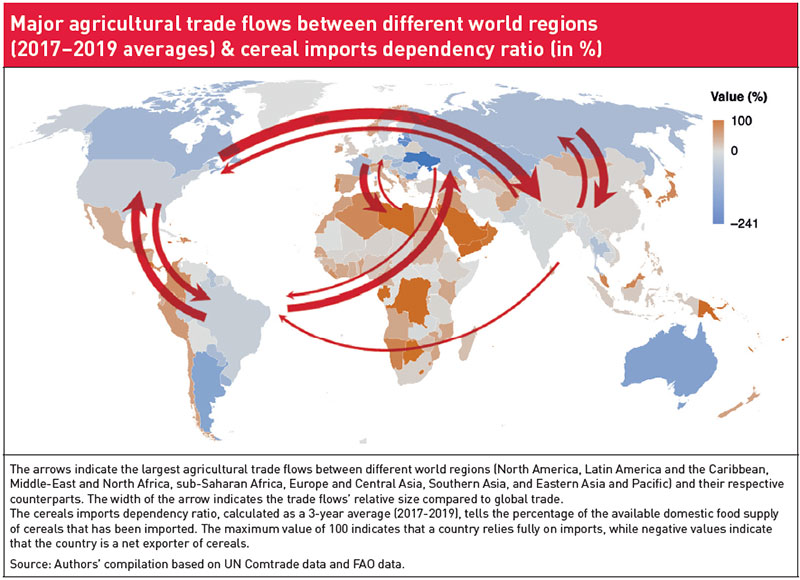

Looking at trade between major trading blocs (see Figure below), half of total agricultural exports is from Europe, Russia and Central Asia, mainly in intra-regional trade. Over a 20 year period up to 2019, there was a shift in trade flows between regions, i.e. a shift to the Global South, while North American exports declined in importance from 19 per cent of total exports to 13 per cent. In East Asia and the Pacific, this pattern was reversed, with exports rising from 13 per cent to 19 per cent in 2019, whereas Latin America's share of exports increased slightly (13 % vs. 15 %) and Middle East and Northern Africa (MENA), sub-Saharan Africa and South Asia more than doubled their share of global exports, contributing to 8 per cent of total exports. This trade pattern was reflected in imports, where East Asian countries also grew. Their share of global imports rose from 20 per cent to 25 per cent, dominated by Chinese demand for soybeans, grains, meat and dairy products. Overall, Chinese imports accounted for 15 per cent of global imports in 2019.

The importance of imports for domestic supply is illustrated by the UN Food and Agriculture Organization’s import dependency indicator (see Figure above), which shows how much of the available domestic food supply of cereals was imported and how much came from the country's own production. The map shows strong differences between regions. Especially the countries in the MENA region and some Central African countries are heavily dependent on agricultural imports. The most dependent countries include the Democratic Republic of Congo (95 %), Libya (94 %), Lebanon (94 %) and Gabon (93 %), which import almost all their needs for cereals. The same applies to countries in Central America and the western part of South America, Japan and South Korea. Ukraine, Canada, Argentina and Australia, on the other hand, are net exporters and net exports amount to 84–242 per cent of the available domestic supply.

Development of world market prices

Prices have an important role in signalling shortages. Price changes are normal in agricultural markets, as supply follows the harvest calendar and yields vary between years. This price movement is regular and can be anticipated. Higher prices help producers cope with low yields, while consumers benefit when prices are low. International trade can typically buffer regional supply shocks. Unexpectedly high and excessive price movements are problematic. Excessive price rises increase market uncertainty and therefore also accelerate inflation and hurt producers as well as the poor, who are typically net consumers and spend a relatively large share of income on food. The consequences are issues of political conflicts and social unrest.

Agricultural and food prices follow a trend that is determined by a complex interplay of various drivers which determine supply and demand in the long run, as detailed below. New technologies and the Green Revolution led to increasing yields, and real agricultural prices (prices adjusted for inflation) have been declining since 1960 for major agricultural commodities – according to the Agricultural Outlook of the FAO and the Organisation for Economic Co-operation and Development, the trend is projected to continue the coming decade. From 1960 to 2000, world market prices for food products, measured by the FAO Food Price Index, followed the trend of commodity prices and decreased, reaching its lowest point in 2000. Since 2000, however, the price trend has reversed, and world food prices have been increasing.

Prices move around this long-term trend, and these movements can be sudden and strong. There have been three major price spikes in the last three decades. In 2007/08, poor yields were exacerbated by the financial crisis, which increased demand for biofuels in response to high oil prices and by speculation, as investors became increasingly involved in agricultural markets. In addition, markets were nervous and protectionist measures led to price increases in markets that were not initially affected, such as rice. After a brief decline, prices rose again in 2011 following a drought and crop losses in the Northern Hemisphere. Most recently, they rose in 2021 in the wake of the Covid-19 crisis, due to disrupted value chains leading to higher transport and fertiliser costs. The Ukraine-Russia conflict further increased energy and fertiliser prices and disrupted key grain and oilseed exports. The effect on the poor is broached in the article "Agricultural prices and food security – a complex relationship".

Temporary price movements are caused by short-term demand and supply shocks, such as weather events, pests and animal diseases, economic and political events. Several factors influence the resulting size of the price spike. One important factor is the general market conditions and the political environment. For example, a well-functioning, integrated and transparent market can partly buffer price shocks, and a high concentration in production lowers the possibility to react and increases the likelihood of severe impacts of market interruptions. High oil prices affect the demand and supply side by raising the demand for biofuels and increasing the costs of fertiliser, energy and transport. In addition, excessive speculation in financial markets, policy reactions such as protectionist trade measures and changing stocks can amplify shocks. The causes and risks of price spikes are demonstrated in the article "Food price inflation, its causes and speculation risks"

Global demand and supply of agrifood commodities

Long-term trends in world food prices are determined by changes in a variety of drivers that can be grouped in supply and demand side drivers, which have changed significantly over time.

Demand side drivers:

The world's population has grown rapidly in recent decades and is expected to continue to do so, reaching an estimated 9.7 billion people by 2050. While some regions are still experiencing high population growth, others are already stagnating or even declining. Three major trends, together with differences in the age structure of populations in different countries, determine the evolution of food demand. In general, more people require more food, and in the rapidly growing populations of developing countries, the proportion of young/adult and productive people is still high or even increasing, leading to above-average demand. In contrast, in many developed countries, the increasing proportion of older people leads to an opposite trend, as older people tend to require fewer nutrients.

Industrialised countries, and in particular emerging economies, have experienced significant economic growth in recent decades, which is expected to continue and spread to other developing countries. This is leading to an improvement in living standards and prosperity. With the increase in disposable income, the demand for food has risen sharply as more people seek access to a more diverse and energy-rich diet, leading to changes in dietary habits with higher consumption of fruits and vegetables, processed and convenience food and meat as well as animal products and the associated increase in demand for animal feed.

Although overall prosperity may increase, income inequality remains a challenge. Some populations and regions may benefit less from economic growth and have limited access to adequate and healthy diets. Other factors contributing to changes in dietary habits and increased demand for food with a wider choice of foods are increasing urbanisation, which is often associated with improved living standards thanks to better access to jobs and services, and globalisation and associated cultural exchanges, which encourage the adaptation of local diets to the so-called Western diet.

Demand changes for food are unlikely to be evenly spread across all agrifood products. Rising incomes and changing lifestyles are driving a shift towards more varied and processed foods, but cereals remain crucial for essential nutrients and calories, especially where they are staple foods. In addition, the growing middle classes in emerging markets may lead to increased consumption of cereals as part of a balanced diet. Cereals are widely used in animal feed production and therefore reflect the increasing demand for animal products. With rising incomes, consumer preferences are shifting towards healthier and more varied food options, including a greater emphasis on fruit and vegetables. As environmental concerns continue to grow, consumers are likely to seek out sustainable food options, further driving demand for fruit and vegetables. Growing demand for plant-based protein is driving the use of oilseeds such as soybeans as a primary source of plant-based protein to meet the greater market for vegetarian and vegan diets.

With rising incomes, consumer preferences are shifting towards healthier and more varied food options, including fruit and vegetables.

Photo: FAO/ Riccardo De Luca

The increasing use of biomass for non-food use in the framework of the bio-economy, especially as an energy commodity, and for feed, raises demand for agricultural products, binds resources and limits the supply available for human diets.

Supply side drivers:

Increases in agricultural production in the past have been driven by an expansion of factor inputs combined with the intensification of agricultural production, such as the use of modern technologies, including improved seed varieties, fertilisers, pesticides and irrigation systems, which have intensified agricultural production, leading to higher yields per hectare and an increase in total food production. More recently, the use of technology and data analysis has led to the development of precision agriculture. Using sensors, satellite navigation, drones and advanced analytical tools, farmers can optimise production, improve resource efficiency and make precise decisions about fertilisation, irrigation and pest control. These specialisations and advances in agriculture have significantly increased agricultural productivity in the past and will play a key role in making agricultural production more efficient, productive and resilient in the future.

However, future food supply is expected to struggle to keep pace with food demand as our natural resources such as land, water and energy are limited, and it is likely that extreme weather events will become more frequent and severe due to climate change, leading to droughts and floods. Land suitable for agricultural production is a scarce factor with limited scope for expansion owing to a growing demand for human settlements or timber. There is also an increasing loss of arable land caused by soil erosion and desertification as a result of climate change. At the same time, freshwater availability is affected by climate change, water pollution and overuse of water resources, which is expected to increase through population growth and increased water consumption in various sectors.

Energy is a key input in agricultural production. Recent events such as the Ukraine-Russia conflict have shown that increasing energy prices affect the cost of agricultural production. The transition to renewable energy and more efficient energy use could help reduce pressure on limited energy resources. Energy costs, crude oil shortages or limited supplies of other commodities such as phosphorus and potassium could lead to higher fertiliser prices and supply constraints, which in turn could result in lower agricultural yields due to reduced nutrient availability (also see article on pages 18–21). Promoting circular agriculture, the efficient use of fertilisers and alternative methods of nutrient delivery to crops could encourage a more sustainable use of fertilisers. Climate change is expected to lead to more extreme weather conditions, such as droughts, heat waves and floods, which could affect crop yields and change growing conditions. Agriculture will likely have to adapt to these challenges, for example by using more resilient crop varieties.

Potential future pathways and the role of agrifood trade

Future pathways to reduce food demand include promoting sustainable diets, taxing and subsidising unhealthy or unsustainable foods, improving food labelling and more consumer education. Increasing food supply can be achieved by investing in agricultural research and development, supporting smallholder farmers, improving infrastructure and implementing land and water use policies that prioritise sustainable agriculture. In addition, waste reduction strategies are needed, such as target setting, donation schemes and consumer education. Improving sustainability also includes promoting organic farming, renewable energy and ecosystem protection. These pathways, together with international cooperation and innovation in sustainable agricultural practices, can help address food challenges and ensure food security.

Climate change, combined with the increased frequency of extreme weather events and the greater likelihood of pandemics and economic shocks, poses a major challenge to food security and the resilience of food systems. International trade plays a crucial role in ensuring food security and strengthening the resilience of food systems. It facilitates the movement of food from surplus to deficit regions, helping to alleviate food shortages and stabilise prices. Trade diversifies food sources, reduces dependence on local production and provides access to a wide range of foods. It also creates access to seasonal and non-seasonal products, contributing to a varied and nutritious diet. International trade facilitates the transfer of technology and knowledge, helping farmers to adopt sustainable and climate-resilient practices. However, increasing globalisation and trade dependence also bring challenges such as trade disruption and environmental impacts. Trade disruptions can lead to supply chain bottlenecks and price volatility, while environmental impacts include greenhouse gas emissions and deforestation.

To maximise the benefits of international trade, it is important to promote diversified and resilient food systems, improve trade facilitation measures, strengthen local production capacity, support sustainable practices and improve global trade governance. Balancing international trade, local production and sustainability is key to building a resilient and secure food system that can withstand climate change, pandemics and economic shocks.

Kirsten Boysen-Urban holds a PhD in agricultural economics. Her research focuses on the links between international trade and global food and nutrition security, and the impact of different policies to support food system transformation for sustainable development. She currently heads the Department of International Agricultural Trade and Food Security at the University of Hohenheim, Germany.

Simon Ehjeij is a PhD student at the Chair of International Agricultural Trade and Food Security at the University of Hohenheim. In his work, he assesses irrigation and infrastructure development and their implications for household food security in Ethiopia.

Dorothee Flaig is a research associate at the Chair of International Agricultural Trade and Food Security at Hohenheim University. She holds a PhD in agricultural economics and her research is concentrated in trade and climate-related policies analysing trade-offs between different SDGs, focusing on economic implications and effects on food security in a globally connected world.

Contact: dorothee.flaig(at)uni-hohenheim.de

References & further reading:

- Food and Agriculture Organization of the United Nations (FAO) (2023). FAOSTAT statistical database. Available online at https://www.fao.org/faostat/en/#data

- United Nations Statistics Division, UN COMTRADE (2023). International Merchandise Trade Statistics. Accessed via World Integrated Trade Solution (WITS). Available online at http://wits.worldbank.org/wits/

News Comments

Current Print Issue

Add a comment

Be the First to Comment