In India, millions of informal hawkers earn a living with small vegetable or

Download this article in magazine layout

Download this article in magazine layout

- Share this article

- Subscribe to our newsletter

Where is food logistics going?

Indian food price inflation was at 10.7 per cent in January 2013. Vegetables, considered a staple food in India, ranged at an alarming 26 per cent in the same period (Economic Times of India, 12.02.13). The media have been focusing on this issue, repeatedly reporting staggering inflation rates in this 230 billion US dollar market and investigating possible reasons for these rises. Public interest in this topic is not surprising. In 2012, the average share of wallet spent on food and nutrition of an Indian household was 43 per cent. Interestingly, while consumer prices are constantly on the rise, farmers are reporting a decline in their production price levels. So the price hikes are mostly due to an increase in the overall margin between farmgate and retail counter. In a straightforward supply chain setup, such as the delivery of vegetables from a peri-urban environment to a city like Bangalore, the capital of Karnataka, a standard markup would be anything between 70 per cent and way above 100 per cent. Note that no packaging, refining, processing or even grading is involved in such a supply chain. The markup is attributable to the relocation of produce from farm to market. According to the media, a simple product such as carrots or bringel passes through the hands of up to seven middlemen before reaching the consumer.

Traditionally, the informal retail sector has enjoyed the protection of the Indian National Government since the days of Mahatma Ghandi. Even today, millions of informal hawkers earn a living with small vegetable or fruit stalls at street corners or in one of many weekly markets, called “mandis”. Acknowledging the limitations and inefficiencies of the existing goods supply system, the Indian Government recently decided to legalise foreign direct investment (FDI) in the Indian retail sector, a move accompanied by fierce public debate, demonstrations and strikes lasting several days.

Whilst there is a certain amount of hope that the market entry of the global players will improve and professionalise the sector to the benefit of the consumer, there is also concern over long-term implications. Will the organised retail chains only put the middlemen in the food trade out of business? Or will they also wipe out street vending and farmers markets completely? Many fear that the traditionally small and marginal farmers in India will be worst hit. Will they continue to earn a livelihood from their smallholdings, or will they be forced to give up and eventually join the urban slum population?

The traditional supply system: not the cream of the crops

Right now, urban retail is extremely dispersed, and not many supermarkets are to be found (Bangalore is said to have the highest organised retail market share at 22 %). At the same time, the country’s agricultural sector is very fragmented. For food logistics, this poses an enormous challenge. Lacking their own transport, farmers are more or less forced to sell their produce locally, making use of a long chain of intermediaries, who will take care of load consolidation, transport, and distribution.

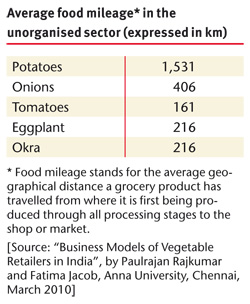

As inefficient as the system might be, average food mileages in India are small, compared to the European Union or North America (see Table above). Tomatoes easily travel more than 800 kilometres in Europe, but not more than 160 kilometres in India. So it is not excessive food mileage, nor exorbitant transport costs, that are to blame for the high markups.

As inefficient as the system might be, average food mileages in India are small, compared to the European Union or North America (see Table above). Tomatoes easily travel more than 800 kilometres in Europe, but not more than 160 kilometres in India. So it is not excessive food mileage, nor exorbitant transport costs, that are to blame for the high markups.

Let’s have a look at the following example: One of the low-cost and high-volume items is tomatoes, with their market price fluctuating between 10 and 50 Rupees (Rs) per kg. Producer prices range at 60 per cent of the retail price. Tomatoes are graded on the farm, packed in boxes and taken to the local Agricultural Produce Market Committee (APMC) for auctioning to traders under the supervision of the commission agent. No further processing takes place until delivery to a retailer in the city. Typically, tomatoes for Bangalore would be grown in an area of up to 150 kilometres from Bangalore city centre, e.g. in the region of Mysore.

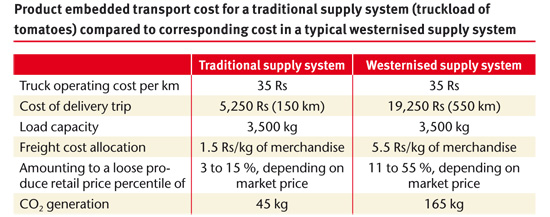

The Table below the allocable cost of transport – in an oversimplified calculation and compared to a westernised supply system. As can be seen, it is not the pure cost of transport which makes retail prices soar. However, the whole process of collecting produce from small farms, consolidating loads, transportation and distribution is rather complex, as will be shown further down. Transportation and handling is both a cost and a time issue. Altogether, this process can involve five to six business transactions and load handling turns. Total delivery time can be up to four days, so the miraculous increase in value of at least 70 per cent is something that could be expected under these circumstances.

It is not surprising that the food wastage percentage in the supply chain is said to be up to 30 per cent. This is produce spoilt through improper storage, improper handling, excessive transportation time and “no sell” stocks, which subsequently go into animal feeding. A big portion of this wastage is a direct result of inefficient logistics and additionally pushes up the retail price levels.

Chain retailing: Will the multinationals bring the solution?

The country’s hopes rest on the multinationals to solve the food supply chain problem. What is certain is that organised retail will bring more efficient logistics and processing, making many of the small traders obsolescent. However, nobody yet knows exactly how this will impact on consumers and farmers. A look at other countries e.g. in Latin America tells us which developments can be expected for the future of India:

Large production units. In the agricultural sector, industrial and mechanised farming will become the norm sooner or later. Small farming will become less profitable, and many independent smallholders will have to give up their land and their livelihood, migrating to cities, or will at least have to opt for contract farming, and restricted independence and autonomy, in the long run.

Processing. Global retailers will prefer to have their product go through a processing chain, starting from quality control and grading, through cold storage, processing and packaging to labelling. Generally, trade margins rise along with the level of processing, with the top profitability items always to be found in assortments such as processed sugar and starch based products, cool drinks and meatstuffs.

Complex logistics. For all retailing chains, the prime competitive factor is company logistics. Logistics concepts which have proven efficient in Europe and the US will probably be rolled out in India one to one. With increased processing, the delivery process becomes multi-stage, meaning that food travels through many stations before reaching the consumer. It is expected that even though the logistics processes will be more professional and more streamlined than in conventional supply setups, the average food mileage is to increase at least by 200 per cent.

Larger outlets in centralised locations. Each of the global grocery retail professionals knows that it is essential to act fast and gain as much market share as possible, say within the first three years of free market competition. This means they will roll out with predesigned strategies, aiming at opening the maximum number of outlets within the shortest time, and at contracting the maximum number and output of suppliers. To achieve this speed, the focus will be on high floorspace outlets in strategic locations.

However, a lot of roadside hawkers being replaced by one large supermarket with a catchment area of say 15 sqkm means a marked rise in the need for urban mobility. Where previously the daily requirements of food and convenience articles could be satisfied by a stroll to the next street corner, now it will mean a scooter, car or bus trip (see Box below).

Generation of traffic demand driven by retail structure

Example 1: In an average suburban fruit and vegetable street market in India, only some 8 to 10 per cent of the shopping is picked up by private motor car, another 15 to 20 per cent by bicycle or scooter, and the remainder is taken home walking.

Example 2: In an average suburban supermarket situation, e.g. in South Africa, assuming a floorspace of 250 sqm, 75 to 80 per cent of the merchandise is shopped by car, with an average one-way driving distance per shopping trip of 1.8 km. With increasing floorspace, the catchment area increases, and with it, the average driving distance per shopping trip.

Fuel dependence and food security. India does not have crude oil reserves, nor does it produce any oil itself. Therefore, all vehicular, processing and refrigeration energy consumption as well as crude oil used for packaging material is imported, bringing about a specific dependency on world markets.

In the final analysis, the setup of the urban food supply lines is also a question of food security and crisis resilience as a whole for the society.

It is also known that for industrialised food production, meat, starch-based and dairy products as well as highly processed sugar products seem to be interesting assortments, whereas fruit and vegetables tend to be high-risk and low-profit, and do not fit well into the standardised logistics processes. Possibly, this trend might – in the long run – even influence the eating habits of the traditionally vegetable-based Indian population.

So while logistics will become more professional, expenditure for packaging, processing, storage and cooling will increase exponentially. At least for processed groceries, food mileage is expected to grow by at least 200 per cent over the traditional fruit and vegetable retailing system. The extra cost will mainly have to be borne by the consumer – although some of it might also be squeezed out of the producers – but the major concern is the question of greenhouse gas emissions caused by the food supply chain, as shown in this example, where levels are more than 3.6 times higher than in the conventional setup demonstrated earlier on.

Compared to the traditional regional supply chains found for fruit and vegetables in India today, the future might bring a setup which could be similar to what we see in the European Union or the United States, with low-value foodstuffs travelling for thousands of kilometres before they reach the consumer.

So, even if the step taken by the Indian Government concerning FDI in the Indian retail sector is understandable, it should be considered as an emergency measure. Like with many other emergency measures, whether it will bring nothing but blessing in the long run remains to be seen.

The best of two worlds: preserve supply chain diversity

India’s population is manifold. Extensive parts of the society can well afford to shop in malls and supermarkets. A member of a ”dink” household, numerous in Indian cities, will stop by at a supermarket on the way home from a highly paid IT job and pick up some ready-made food to be warmed up in the microwave. Only an organised retail can cater for this type of demand. Price levels are not an issue. However, the portion of Indian society depending on low-cost foods can be expected to remain there for quite a while. An alternative supply system should also be kept in place for this market.

So therefore, there seem to be very good reasons to follow a dual development strategy for the Indian food sector. While the organised grocery chains, in co-operation with large-scale farming and industrialised processing, will set up very intricate supply chains for the high- profit assortments, a niche survival market should be earmarked for the traditional system, consisting of small-scale producers and small city retailers, allowing for walking-distance shopping.

Decisive improvements will be necessary to make the existing traditional trading system for fruit and vegetables efficient and competitive. Hopes are that the efficiency of this sector will self-improve quickly, under increased competitive pressure from multinational contenders. So far, however, this has been a fairly unregulated, full-competition market. So, it seems unjustified to raise these hopes too high. On the contrary, the organised chains could wipe out the sector completely, leaving nothing to optimise further. In this case, the low-income city populations would lose a possibility to purchase low cost fresh staple foods in their immediate vicinity, and the society as a whole would enter into a higher dependency on long, complicated and highly fuel-dependent supply chains, which, in the case of a national fuel shortage, might collapse temporarily. The traditional supply structures will have to be nurtured and protected, and innovative ideas will be needed to increase their performance and adaptation.

How can the traditional supply system survive?

Choose the right product range. Relating to certain assortments, such as highly processed and brand foods, the organised retailers cannot be beaten by local supply setups. By contrast, in the fruit and vegetables sector, even small and informal players with little financial clout have a definite chance of success, as the survival of the weekly and farmers markets in Europe and the US shows.

Choose the right geographical setup. So-called “short and regional supply chains” are key to trading in fresh products and perishables and when it comes to preserving the traditional small grower production setup. The prime objective will have to be to organise a local and regional exchange of goods and to make the growers in the immediate geographical vicinity of the agglomeration independent of traders or middlemen.

This is easy to do in the urban vicinity, but gets very difficult in remote areas. Therefore, giving preference to vegetable production in the peri-urban areas makes sense and might eventually result in the formation of “urban vegetable belts”. In the long run, these would double up as an emergency food reserve for urban populations.

Enable a high-performance logistics setup. Whereas farmers in Europe and North America supply to weekly markets directly, using their own vehicle for the shed to market delivery, most Indian farmers have not progressed to this level, yet. Without their own transportation, they can only depend on traders and middlemen, which counteracts the notion of logistical efficiency. Even where goods are transported directly from the village to a city, this is done in minute quantities on motorbikes and tricycles, a both uneconomical and unecological practice that creates enormous traffic problems in the cities (see Box at the end of the article).

The key question is whether traditional and regional supply setups, even after adoption of innovative logistics concepts, will be able to resist high-powered competition from organised retail. In India, we will have the answer in just a few years’ time. However, looking at the development of fuel prices, some people consider intricate, transport-intensive food supply chains as being transitory, and expect local and regional food supply to come back either way – all a question of time.

The impact of logistics on urban traffic congestion and GHG emissions

Bangalore consumes some 2,000 tonnes of vegetables a day. Depending on whether this volume is shipped on trucks or auto-rickshaws, as is often the case today, the impact on the network traffic load and the environment can differ considerably. With haulage by regular trucks, this flow of goods represents some 600 truckloads, taking up approximately 9,000 sqm of traffic space at any one time, and generating 27,500 kg of CO2. If auto-rickshaws or other small vehicles are used for transportation, with an average load of some 130 kg (e.g. a full microvan load for tomatoes), some 32,000 sqm of traffic space would be used and 105,000 kg of CO2 would be generated in the operation.

Bernhard Herzog

Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH

Eschborn, Germany

bernhard.herzog@giz.de

News Comments

Current Print Issue

Add a comment

Be the First to Comment