Delivering milk to a collection centre in Tanga, Tanzania.

Photo: ILRI

Download this article in magazine layout

Download this article in magazine layout

- Share this article

- Subscribe to our newsletter

Linking poor livestock keepers to markets

An estimated one billion poor livestock keepers live in developing countries. About 600 million are found in South Asia, mostly in India. Sub-Saharan Africa has more than 300 million poor livestock keepers, mostly in East and West Africa, but also in the Southern and Central regions. Livestock keepers derive various benefits from their animals, starting with food (milk, meat, eggs) and services (draught). They also earn income when selling livestock or livestock products. Manure used as natural fertiliser is crucial for soil fertility management. Finally, livestock are used as savings and can be sold to get cash in case of an emergency, and in many setups, livestock also provide important social benefits.

Market orientation is low, with many livestock keepers operating at subsistence level with no or limited surplus to sell. On the other hand, demand for animal source foods is expected to increase annually by 2.8 per cent in Africa and 4.1 per cent in South Asia between 2007 and 2050, due to population growth, increased income and urbanisation, a phenomenon known as the Livestock Revolution. The question is therefore whether smallholder livestock keepers are going to meet the demand by increasing their productivity and being able to generate a surplus. Better off and larger-scale producers may be in a more favourable position to respond to this increase in demand, especially as consumers are increasingly demanding safer products. On the other hand, linking small-scale farmers to livestock markets not only makes economic sense, since they have been shown to have a comparative advantage in livestock production, but also addresses the issue of equity. This article first describes reasons why livestock keepers are weakly linked to markets. We then present some approaches that have been followed to strengthen livestock keepers’ access to markets.

Why do livestock keepers not access markets?

Access to market refers to input and service markets on the one hand and output markets on the other. Although in some systems, livestock keepers are able to increase productivity, and therefore sale of outputs, using their own resources (e.g. land/ labour), in most cases, farmers will need to purchase external inputs (like feed) or services (to maintain their animals’ health) to generate a surplus. A value chain approach that looks at the various actors, from input and service providers to final consumers, is needed. Indeed, previous projects that focused on only one part of the value chain, for example production, have often failed as other bottlenecks along the value chains had not been considered at the time.

Reasons for low market orientation include unavailability of a reliable and/or profitable markets as well as low surplus, either because of low production or a high consumption level within the family unit. For any livestock keeper to invest resources, including her own family labour and land as well as financial resources, to generate a surplus, she must be able to sell her products at a price that is above production costs. Smallholders’ market orientation has been reported as low, especially among pastoral communities (McPeak and Barrett, 2001). In areas suitable for dairy farming in East Africa, a survey conducted in 2009 shows that only half the cattle keepers sold milk on a regular basis. On the input side, the same survey data show that purchase of inputs was even less frequent: only 5 per cent of dairy farmers in Rwanda bought dairy concentrates. The percentage was higher for Uganda (33 %) and Kenya (58 %). Purchase of fodder was even less frequent, with 5, 15 and 17 per cent of cattle keepers doing it on a regular basis in Uganda, Rwanda and Kenya respectively (EADD baseline reports 1 and 3, 2010).

In the past, some inputs and services like artificial insemination, veterinary and extension services were heavily subsidised, and therefore their use was relatively high, with a positive impact on productivity. Structural adjustment programmes in the 1980s meant that most governments had to cut on support to these productivity enhancement initiatives. The objective was that the private sector would move in and bridge the gaps. However, this is only happening in the more intensified, livestock-dense areas, where it will be profitable (Owano et al.). In other areas, in particular in the pastoral areas, such a development has not been observed much.

Three approaches

Various approaches to link livestock keepers to markets have been followed, and in this article we look at three of them. The first two describe experiences linking farmers to local (national) markets, one based on collective action and the other on contract farming. The third example is about export markets.

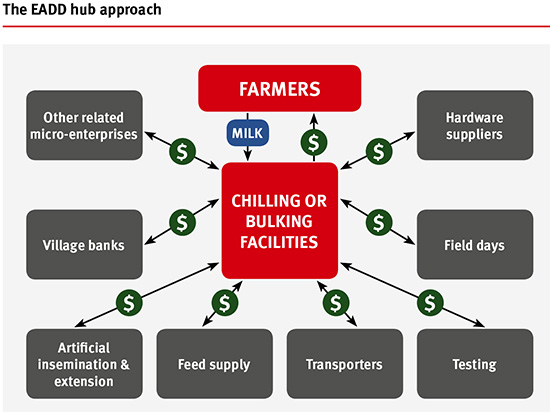

Linking farmers using Producers Organisations – the power of collective action. Producers Organisations (PO) are at the heart of the hub approach, which is a mechanism to upgrade the value chain by facilitating market linkages. In situations where smallholder producers are scattered and produce low volumes, it is uneconomical for input and business service providers (e.g. feed inputs) and traders/ processors (e.g. milk traders and processors) to provide services to these farmers. A hub approach will start by identifying the organisational and institutional arrangement(s) required for farmers to get together (through, for example, a co-operative) and supporting the group in moving toward this desired state. At the same time, market agents are sensitised and supported to provide business linkages to the PO. By working with the private sector and building the capacity of producers to run and own their organisation, this approach aims at ensuring sustainability of the market linkages when project support ends. The value chain transformation is possible when there is a win-win situation for most of the value chain agents, including women and men producers. The Figure on page 24 describes the various inputs and services that cattle keepers can access through their POs.

The approach has been successfully promoted by a range of development partners, in both crop (e.g. coffee by TechnoServe) and dairy. Focusing on the dairy value chain, the approach has been followed in three countries of East Africa (Kenya, Uganda and Rwanda) during the first phase of the East Africa Dairy Development (EADD) project. Increasing poor livestock keepers’ access to markets though the hub approach has had a positive impact on productivity and income. Indeed, active suppliers of producers organisations supported by EADD have seen an increase in milk productivity in their cross bred animals of between 50 and 60 per cent depending on the countries, with the largest increase recorded in Kenya. In Uganda, we also observe an increase in milk yields among local cattle. Even though difference in methodology between baseline and final evaluation prevents clear comparison, overall, there has been an increase in dairy income in nominal terms for the three countries and in real terms for Uganda (between 30 % and 130 %). For cattle keepers to have long-term access to markets, beyond a project support, the team developed a tool that assesses the PO’s progress towards sustainability using both production and business dimensions, for example its ability to run Board elections regularly and freely or PO members’ ability to access feed inputs on credit. A Producers Organisation ‘graduates’ when it reaches a certain score (60 %), meaning that external support, from development partners, is no longer required. Data have shown that on average, it takes 7.3 years for a PO to reach ‘graduation’. Sites in Kenya and Rwanda have progressed significantly faster than Ugandan sites, while pre-existing sites have done so much faster than all the other hub types.

In other settings, productivity levels are low, and the research question is therefore whether the hub approach would be applicable in areas with little marketable surplus, with the first intervention point being increasing access to inputs and services to improve productivity. The approach is being tested in the pre-commercial areas of Tanzania as well as in other livestock value chains, including the pig and small ruminants value chains.

Contract farming. In many cases, contract farming is seen as a useful way for smallholders to get access to both inputs and output markets in Southeast Asia, but looking at evidence, the history of contract farming for livestock is mixed, and is characterised by various institutional arrangements, based on local conditions. In the case of pigs and pig meat value chain in northern Vietnam, Lapar et al. (2009) show that there are various possibilities for pig producers to access markets: they can engage in formal contracts with integrator companies or in informal contractual arrangements with co-operatives or with traders of inputs or/and of outputs. Smallholders usually find it difficult to enter into formal contract arrangements because of barriers due to scale: integrators offering formal contracts require relatively large-scale operations for efficiency purposes and to reduce monitoring costs (it is easier to monitor and supervise a few large farms than numerous small farms). Smallholder farms therefore need to find other mechanisms to access markets.

For the same reasons as integrators, traders also prefer larger-scale producers. It would therefore be important to examine the potential of co-operatives to facilitate profitable pig production by smallholders, as well as looking at the broader issue of product certification and infrastructure that smallholders can access and have the quality of their pigs assessed and certified (particularly for disease-free status or lean meat content) by according to specific grading standards. A partnership between large farms/companies and smallholder pig producers can also be envisaged, for an inclusive value chain approach.

Export markets – the case of Namibia and Botswana. The cases of the beef sectors of Namibia and Botswana are examples of livestock keepers succeeding in accessing high-end retail European markets. Both countries belong to the African Caribbean and Pacific Group of States, and like its other members, they have had historical preferential trading relations with the European Union under the Lomé-Cotonou agreement, now being reformed into the Economic Partnership Agreement (EPA). Namibia is among the top ten beef exporters to the EU, and it managed to penetrate the high-end niche markets in Europe. By shifting from marketing beef as a commodity to a smart branding and marketing strategy of selling their key beef attributes (e.g. free-range, hormone free, animal welfare), Namibian beef exporters have realised higher returns in revenue and in turn offer higher prices to producers. Key to this success has been the implementation of a credible individual cattle identification traceability system. Botswana, on the other hand, has been an inconsistent supplier due to export bans related to a weak traceability system and frequent outbreaks of foot-and-mouth disease (FMD). While in both cases, smallholder livestock farmers are able to supply this high-value channel, the extent of their participation is lower due to the high costs of compliance, frequent changes in EU standards, FMD control challenges, and the lack of land titles to secure bank loans that can enable them to add value to their livestock. As such, a mixed approach of market segmentation that strategically targets high-end international markets while also capturing regional market opportunities is more sensible. This can lead to a more inclusive livestock development.

The way forward

There is no ‘one-size-fits-all’ approach to link livestock keepers to the market in a manner that is inclusive and sustainable. Women’s and men’s needs have to be taken into account for a value chain transformation to happen. There are still many unknowns, in particular regarding the effect of increased market orientation on the household nutritional status. In fact, the effect can be negative when more livestock products (like milk) are sold rather than consumed at home, extra income is spent on items not beneficial to children health and nutrition, and women’s workload increases and less time is available to care for their children. Concerted efforts by researchers, development partners, public and the private sector are needed for inclusive value chains to become a reality so that poor livestock keepers can take advantage of the Livestock Revolution to improve their livelihoods in a sustainable manner.

Isabelle Baltenweck

International Livestock Research

Institute (ILRI)

Nairobi, Kenya

i.baltenweck@cgiar.org

News Comments

Current Print Issue

Add a comment

Be the First to Comment