In tea production, small-scale processing structures coexist with larger ones.

Photo: J. Boethling

Download this article in magazine layout

Download this article in magazine layout

- Share this article

- Subscribe to our newsletter

Large-scale agro-processors in sub-Saharan Africa: A catalyst for pro-poor growth?

Agro-processing (and other post-harvest treatment of agricultural products) is one of the four pillars of agro-business, together with agricultural input supply, machinery and equipment, and services such as finance and trade. In many agro sub-sectors, a trend towards larger units is observed (according to the United Nations Industrial Development Organization UNIDO, an enterprise is considered large if it has more than 100 employees in developing countries and 200 in developed countries).

The reasons are manifold, coming from different sides – consumption, production, and the economic and regulatory framework (keywords: super-marketisation, demand for processed and convenience food, economies of scale, technological progress, fixed costs, health, environmental and social standards and regulation, traceability). These factors are particularly at work in processing for industrial products, but also in many food mass markets.

Trends of large-scale agro-processing in SSA

Large-scale processing, at least in terms of a first processing stage, is common in many export-oriented value chains (e.g. cotton, vegetable oil, sugar) since economies of scale, the structure of concentrated demand of second-stage processors and retailers as well as regulations and standards in the final destination markets support size. In some markets, such as the classical tropical products coffee, cacao or tea, first-stage small-scale processing structures coexist with larger ones, and their semi-processed outputs are channelled through systems of standards and auctions towards the large processors in the North.

In contrast, markets for locally procured and processed food products are still dominated by small, often informal actors. It is estimated that 60 per cent of the African labour force are at least partially involved in small-scale food processing, most of them women. This can be explained by the historical underdevelopment of several of the above-mentioned demand factors, in particular low urbanisation, low household incomes and, thus, low demand for processed, branded, standardised food products. In addition, supply problems are important: the procurement of large amounts of agricultural products of standard quality and in a timely manner in SSA is difficult due to many reasons: small farm sizes and dispersion of producers, lack of reliable marketable excess production due to numerous difficulties of smallholder farmers, low number of functional cooperatives or other types of farmer groups, shortage of advanced production technologies, absence or non-respect of standards and regulations, information problems and other high transaction costs in rural areas and along the food chains.

With the gradual change of local food demand and markets (keywords: high growth rates, new middle class, record urbanisation), the situation described has started to change at the demand and retail level. Large supermarket chains have been observed to make a dent in urban markets since the 1990s, particularly by South Africa, which has a strongly developed industrialised food market and an active expansion policy. South African companies are said to control 80 per cent of the processor sector in SSA. But also, some local companies and those from other nations have become active.

However, the above-mentioned strong supply side problems in sub-Saharan Africa (SSA) suggest that, even where demand for industrialised processed food products arises, this is often served more easily by importing processed food than by processing of locally procured commodities. But importing food is often costly, does not allow an exact fit for consumer preferences, and is further handicapped by trade and food regulations. Thus, large local retailers have increasingly tried to procure locally. This has opened up opportunities for the processing industry. Another important driver for this trend is a change in perception of risks and opportunities of doing business in Africa generally. Some public policies and investments are supporting large processors in particular: the abolishment of internal trade barriers, regional and continental trade agreements, infrastructure and communication, common standards and protocols, reduction of bribery at customs, trade facilitation, transnational financial services, and the like.

In summary, agro-processing investments by both international foreign direct investors as well as local companies have been found to increase progressively since the mid-90s. Cross-border mergers and acquisitions in the food-processing industries in Africa increased from 27 million US dollars (USD) in 1991/95 to 1,400 million USD in 2007 (almost 13 % of all developing countries). Foreign investors targeted rice, wheat and oil crops as well as sugar and floriculture in particular.

The food price crisis in 2007/08 and the rising agricultural price trends since then have certainly played a major role in incentivising investments in the African food sector in recent years: they have renewed the attention for natural resources and agriculture, and SSA has been discovered as the single largest potential pool of as yet underdeveloped natural resources for increasing world food production. The rush for agricultural land by international investors is an indicator of that perception. While these are strongly debated, large agro-processors receive less criticism, and many policy-makers and donors see them as important instruments for a modernisation of food value chains, securing supply and reducing poverty. Currently, thus, a new wave is emerging of agro-business interest for, and in, SSA, often supported by donors.

Different models of interaction: impacts and risks

There are several fundamentally different ways how large-scale agro-processors may interact with and impact on national economies. One strain is through products and prices on consumers, one is with competing small-scale processors, another is on suppliers, and yet another is linked to the political economy of the food sector.

Arguably, the most important strain is with suppliers, in particular farmers, because the presence of large processors changes several fundamentals in the relations, rules, logics and power structures within the food value chains. The number of producers in a food value chain is much larger than the number of direct employees in the processing industry. For instance, in the European Union, for which the numbers are readily available, more than 80 per cent of food, beverage and tobacco sector employment is in agriculture, and less than 3 per cent in manufacturing, though the value addition of each is about 25 per cent. The mode of commodity production – large or small-scale farming – will also strongly influence the environmental impacts.

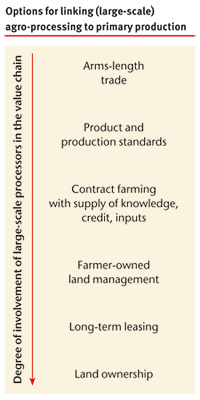

There are several ways (large-scale) to link agro-processing to primary production. These reach from arms-length trade on anonymous markets to complete control of procurement on fields owned by the businesses themselves (see Figure above). Which form is appropriate, preferred and finally realised depends on many factors, several of which are under the direct control of the processors. The United Nations Conference on Trade and Development (UNCTAD) has developed the OLI paradigm to classify factors into: Ownership-specific advantages of a large corporation to produce a certain good, Locational factors that specify production and investment conditions of a specific country and site, and considerations to Internalise operations (or to licence or contract them out). Although this concept allows for a very broad categorisation of factors and a reflection of issues such as supply capacities, market and regulatory requirements, some issues in farmer-processor relations in SSA warrant special attention.

- As indicated, supply-side weaknesses of smallholder agriculture explain why and experience tells that arms-length trade is rarely able to satisfy the demand of large-scale food processors.

- One particularity of agricultural value chains is that land is a very special kind of investment good that is especially delicate in SSA due to its social, legal, political, ecological, cultural and even religious properties. The observations around the new rush for large-scale land acquisitions and the global public outcry, contrary to most other forms of investment, demonstrate this uniqueness. In addition, agricultural cultivation does not regularly show strong economies of scale. More capital, better production technology and input use of large cultivators are often more than compensated by disadvantages in labour surveillance, risk and management costs. Smallholders are more flexible, and can exploit cheap family and local informal labour and crop at the margin. They are small, vulnerable and poor, but efficient.

- Another particularity in SSA is the historic legacy which still strongly influences present agri-food structures. Many present-day agro-processing enterprises have derived from privatisation of former parastatals in the frame of Structural Adjustment Programmes (SAPs) and further mergers and acquisitions. These structures have established deep-rooted habits, dependencies, institutions and policies. Thus, there is quite a strong path dependency in some sub-sectors.

- In summary, large agro-processors are torn between centrifugal, centripetal and stationary trends when considering whether or not to get primary production under their direct control. In many cases, a not completely integrated model will be the best (available), where farmers have to be supported in one way or another, by organising them, by providing training beyond public extension services, or by supplying additional services, inputs and credit in the frame of a contractual arrangement (see article: Engaging smallholders in value chains: who benefits under which circumstances? ). If supply is risky and circumstances are unfavourable, an agro-processor, particularly one with high fixed capital investments, may even want to produce a larger share of the primary products himself. This is the rationale for large-scale land acquisitions by many large-scale processors. In sugar, for instance, a rule of thumb is 70–80 per cent of one’s own production to protect an investment which can easily reach a hundred million USD.

Successes and failures

Looking at the present developments of old and new processor-smallholder interlinked models, the balance is quite mixed. After SAPs, privatised agro-processors could, in some cases, strengthen their efficiency, often by adjusting (formerly excessive) jobs, wages and other costs (e.g. sugar estates and mills). Some disappeared (many government-controlled cooperatives or tomato processing in West Africa) or could only be rescued with additional government interventions (e.g. cashew in Mozambique). In many instances, a long series of adjustment steps took place, successively disentangling and dismantling the many functions of integrated state-controlled structures, and often in an attempt to rescue the core large-scale business. In yet further cases, government (co-) ownership continues to exist (e.g. in cotton ginneries in several West African countries).

The few more recent investments are showing mixed success, too. Export horticulture global value chains starting from a few SSA countries, which include some processing, are success stories in Kenya and Ethiopia but less so in West Africa (although there are some). The supply of local supermarkets and related formal food chains is often successfully taking place in fresh fruit and vegetable products, for instance, although these are frequently specialised medium-size enterprises, given the still small volumes on national markets. However, there are a few successful large-scale ones, often connected to export chains. In contrast, the first wave of biodiesel producers, mostly based on the Jatropha plant, whether from their own plantations or from smallholder production, largely failed all over SSA, for a number of reasons including low experience, a wrong business model and/or (wrong) interventions (or lack of them) by governments.

Farmers have been strongly affected by changes, successes and failures of agri-processor structures, although it is often difficult to disentangle processor-specific issues from wider sub-sector reforms in the complex SAP-related processes. In some instances, the SAP liberalisation was beneficial, achieving higher prices through high efficiency in processing but also through some other channels (trade, exchange rate, price policy). However, in a number of cases, the guaranteed outlet to a processor had been important in stabilising prices and gaining access to technology, training, inputs and credit. Farmers lost these advantages with the disappearance of the monopsonist, since smaller buyers have not delivered these, either for lack of their own access or because the side selling (risk) overwhelms all advantages of fostering supply in the remaining atomised market structure.

Experiences further show that private large processor companies in the agricultural sector are no easy political partners. There are risks of unfair contractual relations with farmers, manipulation of competition and trade policies, etc. In SSA, this is accentuated by a low level of capacities of state authorities to create a level playing field for making business and imposing contract execution, as well as widespread corruption. This must not necessarily be unfavourable for farmers and workers, but for consumers and overall welfare.

Conclusions

Large-scale agro-processors face very different situations in SSA, depending on the products and markets. Though some exist for a long time, conditions are generally not favourable for them. In the longer run, however, they are projected to grow due to long-term trends in demand, technology, markets, policies, regulation and private standards, both for export and for internal markets. Africa would be forfeiting some market segments if it were not adjusting to accommodate them. Policies can partially shape the occurrence, behaviour and impacts of large-scale agro-producers, but they are difficult partners in the generally small economies with weak business partners and weak government structures.

Private-Public Partnerships (PPPs) within a strategic framework of improving entire sub-sectors nationally or regionally may work best to create appropriate spaces for new large-scale processors. Some of the new alliances emerging seem to endeavour such PPPs. However, given the complicated nature of procurement and land ownership structures in SSA, the most important partners will be farmers, and they will also widely determine the overall social impact of such partnerships (though competing small-scale processors and consumers should not be forgotten). Thus, they should be full-fledged partners in the emerging coalitions, or Peasant-Public-Private Partnerships (PPPPs). These will be faced with many difficulties due to very different characteristics in terms of social, informational, technical, financial and power attributes and different time horizons, expectations and goals. The state, and particularly donors, have to handle the difficult role of assuming a facilitating, neutral role, letting the private partners negotiate and carry out commercial activities, while at the same time supporting the weaker partners – the farmers. In addition, they may supplement infrastructure, materials, technology and services that are in short supply and beyond control or capacities of the private partners.

On a more general level, care has to be taken how to balance the roles of such large players within the entire food sector. Though there may be trends towards products and value chains in which large-scale processors have a comparative advantage or are even the only feasible option, most of SSA’s food markets are and will be dominated by more informal value chains and channels now and for a long time to come. These can be very efficient, they are often the better choice in social terms, they are less problematic in political economy terms, and they can improve. Support for this part of the food chains is possibly more complex, but also worthwhile, including through regulation of large actors. To select the right balance between the different segments and actors is certainly a very important and difficult task. The insight that most SSA countries are not yet ready to design and implement good industrial policies for the general welfare must give rise to concern. However, not reacting will not be the better option – thus, an attempt must be made to ride the dragon.

Dr Michael Brüntrup

German Development Institute/

Deutsches Institut für Entwicklungspolitik - Bonn,Germany

michael.bruentrup@die-gdi.de

News Comments

Current Print Issue

Add a comment

Be the First to Comment