Input credits are granted for some cash-crops, especially if this can check side-selling via monopoly marketing – for example for cotton-growing in northern Benin.

Photo: Michael Brüntrup

Download this article in magazine layout

Download this article in magazine layout

- Share this article

- Subscribe to our newsletter

Supply chain finance – a viable option for smallholder farmers?

Access to finance continues to be a major problem for farmers in developing countries, especially in sub-Saharan Africa. The lacking availability of agricultural credits is seen as a central, if not the most important, obstacle to the expansion, modernisation and diversification of production and the adoption of innovations. A more recent, very detailed analysis of national operating data for four countries in sub-Saharan Africa by Serge Adjognon and colleagues demonstrates that while 70 per cent of all farms in Malawi and Nigeria buy fertiliser, pesticides and seed as external inputs, a mere 16 to 18 per cent do so in Tanzania and Uganda, showing relatively few systematic differences regarding farm size (in all four countries, the smallest farms, with less than 0.5 ha, have the lowest use rate). But an average of just 6 per cent (3–11 per cent, depending on country and farm size) purchase on credit, mainly buying fertiliser, and almost everywhere, except for Nigeria, the medium-sized and large farms acquire significantly more on credit than the small ones. So there is an urgent need for more financing, which also has to be more diversified.

However, farmers tend to be difficult financial clients. Owing to their exposure to collective weather and other natural and economic crises, they are seen as particularly risky borrowers. Low levels of formal education and literacy rates make information and counselling on financial and business management matters a complicated issue, as does the provision of good planning documents for granting credits. Usually, farmers also have few material collateral, and even in the case of mortgages on registered land and other real estate titles, it is often difficult for lenders to liquidate such collateral in rural areas. Given the frequently large distances, the transportation, information procurement and other transaction costs are high anyway.

Supply chain finance – pros and cons

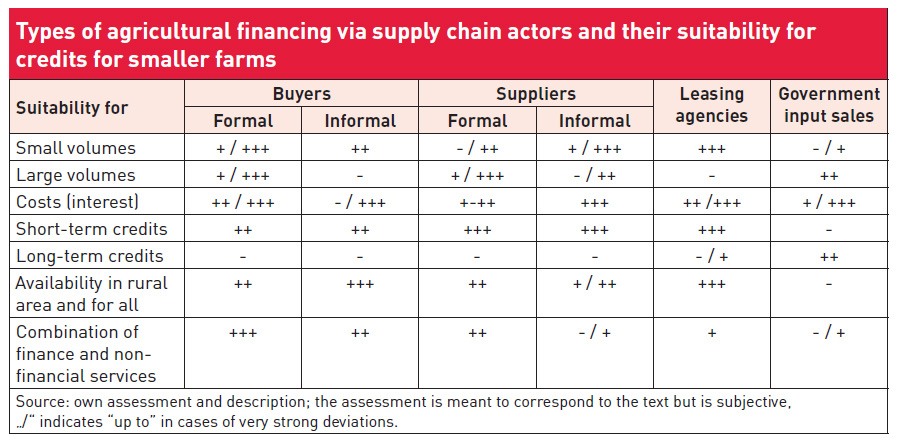

For all these reasons, pure financial organisations of the most various kinds (banks, microfinance organisations, finance cooperatives, savings banks, etc.) have difficulty or little interest in adapting their business models to the special needs of farmers and their production processes. This is why a number of other financing models have evolved providing products, services or finance which do not reach the farmers via financial service providers but via actors in the upstream and downstream areas of agriculture. They are referred to with the generic term of supply (or value) chain finance.

There are a wide range of models, although they do share some common features. Supply chain financers dispose of a good knowledge of cultivation, products, markets and services which are important for farmers. They also take an interest in the goods or services purchased being of high quality, and can partly influence or guarantee the latters’ quality. In many developing countries, lack of quality constitutes a major problem, and farmers have hardly any options to control quality. One further advantage of major economic actors in particular is that they frequently have access to international financial markets with (at least in the past) favourable interest rates and make these available to farmers. The general disadvantages are that under such systems, independent markets for the upstream services do not develop so easily, that farmers become even more dependent than is already the case, and that the real-term credit costs lack transparency owing to their being subsumed under other costs. Such credits are usually not covered by financial market regulations, even though they can be quite relevant to the financial system given their aggregated dimension. Depending on the lenders, interests and relationships with the farmers tend to vary.

The demand side

The purchasers of agricultural products offer pre-financing of inputs, interlinked credits or tied credits, usually in the context of contract farming. Credits for inputs are frequently provided in kind in order to cushion risks on the input markets and safeguard production. One big advantage of obtaining credits via buyers is that the latter are familiar with the requirements of the sales markets, especially if they themselves are active in cultivation (e.g. nucleus-outgrower schemes). Often, the credits are then part of entire packages of financial and non-financial services, including the prices or price-fixing regulations for the products being sold. Everything is financed through marketing and its margins. One core problem of the model is so-called side-selling, which refers to being in breach of delivery contracts by the farmers, and hence the risk of non-(re-)payment of credits and other services. Non-compliance with price-fixing or other agreements on the part of the buyer can be a reason for side-selling, but so can more attractive prices and purchasing terms of third-party buyers. In all cases, a partner’s short-horizon thinking encourages this form of granting credits.

Where monopoly situations or the special structure of a cash crop sector encourage this, marketing boards (still) exist. The monopoly situation hardly allows for side-selling, which makes granting and repaying credits easier. Sometimes, a farmer can also use the cash crop guarantee (e.g. cotton) for another crop (e.g. maize). These boards were widespread in developing countries between the 1960s and 80s, often encompassing all functions of the subsectors or even the entire agricultural development in a region. However, for similar reasons to those in the case of specialised agricultural banks (see article "Towards a renaissance of agricultural development banks in sub-Saharan Africa?"), they were very frequently ineffective and not sustainable financially, at least under the then prevailing conditions of one-party governments taking advantage of these organisations to steer the economy, siphoning off agricultural profits and, often enough, radically exploiting the farmers. Therefore, most of the boards were done away with in the course of structural adaptation measures. If they do happen to have survived (for example for cotton in many West African countries or cocoa in Ghana and Côte d’Ivoire), their roles and their power have usually been reduced. Therefore, longer-term credits and extensive non-financial support is rarely provided nowadays.

Such contract-farming arrangements on a usually smaller scale also exist in private sector value chains. Owing to the problem of side-selling, they either focus on certain cash crops for which there is either a local private monopoly or where the product can be bought at a higher price than the local market price (in niche markets such as fair trade or organic agriculture). Buyers with high investment and fixed costs (processors), of highly perishable products (logistics costs), low availability on the free market (dependence on producers) or sophisticated buyers (penalties for breach of contract, risk that non-fulfilment of contracts will lead to the end of commercial relations) are also more inclined to enter contract farming and grant credits. Or the credits are based largely on trust, experience and safeguarding within social networks. The already referred to multi-country survey mentions such credits on an extensive scale for tobacco and partly also for cotton, but otherwise, cash crops do not benefit more frequently from credits than food products.

Most supply chain credits consist of labour only paid for after the harvest –

here, soil is being tilled to grow yams in northern Benin. Photo: Michael Brüntrup

The supply side

The providers of upstream products and services can also grant credits for the purchase of their products, and this is then mainly done directly in kind. These credits are usually repaid during or after harvest, sometimes by an already contractually agreed retrieval at source when the farmers are paid for their products.

Specialised suppliers such as the fertiliser industry have a restricted range of products from which individual farmers only need small amounts. However, they require various products and services at very specific times during the planting and growing season. Often, specialised agro-dealers or farmers’ organisations compile the products needed and see to the “last mile” of delivery. Whether these middlemen offer credits or allow buying on credit depends on the financial capacities of the traders and trust, transparency, formal legal security and whether debts can be legally recovered. Even in these local business relationships, social pressure plays an important role in fulfilling obligations.

Purchasing cooperative societies reduce some of the transaction costs and provide better negotiating power. They can also compile customised product ranges from individual suppliers. Social pressure to observe payment discipline is considerable. However, these societies do bear the familiar problems of cooperatives: they are slow in decision-making, have a tendency to exclude the poorest, are sometimes little bankable and are often less innovative and financially strong than purely private enterprises.

Leasing agencies now and then devote their services to agriculture, e.g. for tractors and machines. As yet, they only rarely occur in rural regions, one example being the KfW-financed Equity for Africa Group in Kenya. Leasing agencies are not necessarily cheaper, but they do reduce the considerable procurement costs to regular, smaller payments in instalments, which of course in farming have to be synchronised with the seasonal cash-flows. In order that the leased investment goods can serve as guarantees, training has to be offered and a legal framework has to be in place. Furthermore, a second-hand market must exist for further selling off.

One special form of supplier credits is labour with wage payment postponed until after the harvest. It is much more widespread than credits for input – the study referred to above states at least 20–30 per cent of farms in Nigeria and up to 50–80 per cent of farms in Uganda, across all farm sizes in all countries. This confirms that, at least at certain times, labour is a key factor which is hard to come by for farmers. Moreover, delayed payment backs the hypothesis that massive credit access problems exist for farmers. The workers are probably among the poorest of the poor (landless people, micro-smallholders, households experiencing acute difficulties). One special case is direct government sales of input and investment goods. In many African countries, following the example set by Malawi, fertiliser subsidies have been introduced since the mid-2000s. Strictly speaking, these are not usually credits, but strongly reduced prices for certain items, although they often facilitate credit granting by the private supply chain partners of the farmers. However, tractors, machines and even entire processing plants are still directly supplied by governments (or by development organisations) on credit. Many studies report very poor repayment rates for products financed by government credits.

Some final reflections

The requirement for more agricultural financing which is also more diversified is huge in poor developing countries. The demands on agricultural financing are complex, and there is a very wide range of needs. And yet, the financing of other supply chain actors whose profiles of needs are often very different has not even been referred to here. If they are underfunded, entire supply chains and hence also farmers often run into difficulty, or a supply chain might not even evolve.

Each of the different supply chain models has its own advantages and disadvantages, usually depending on the context, the products, supply chains, market power, competitive situation, regulatory framework, etc. But basically, supply chain financers cannot and do not want to provide general and multi-purpose financial services but necessarily seek to above all promote their own supply interests. As long as finance independent of supply chains is available, supply chain financing is not objectionable, it then constitutes one funding option among several for farmers rather than being the reason dominating all other crucial factors to consider for entering a certain type of production. And then well-adapted supply-chain financing, if possible in a well-adapted package, can make use of its advantages to the full. If this is not the case, efforts ought to be made to develop alternatives which allow credit directly from financial organisations. Development cooperation interventions and political regulation can contribute to this.

Development cooperation can seek to ensure that financing of farmers is at least partly secured via financial organisations (FOs) in promoting supply chains and in private sector and financial sector programmes. This can for example be achieved by supporting triangular cooperation schemes in which payments by and to farmers are performed via their own FO accounts. Once the money is in one’s own account, saving becomes simpler. Then farmers can develop their own savings and credit record, which is an important criterion for FOs granting their own credits. At least partly cashless transactions are also preferable from a transparency and security angle.

Certain constellations can also be influenced in supply chains via political interventions. They are legitimate and often necessary to make up for the multitude of imperfections and failures in the finance and agriculture sectors of developing countries. Many actors such as farmers or groups of farmers, smaller suppliers and buyers as well as supporting structures like rural communities are often weak and poorly organised (another result of high rural transaction costs) and have little political and economic power to act. In some chains and sub-sectors, they face all-powerful private individual actors in national and international agro-business, and this can perhaps also constitute a case for regulation.

For these and many other reasons, the agricultural sector is often shaped by strong regulations which in turn have to be considered in financing. For example, this sector is more strongly affected than others by considerable government interventions in trade, food security and the environment. Pricing policies for inputs and crops as well as the choice of distribution systems can massively change the preconditions for agricultural financing, for example when pan-territorial prices are set (which reduces the risk of side-selling), when trade policy stabilises prices (reduces credit risks) or destabilises them (raises credit risks), or when subsidies are handed out in the shape of government distribution of goods (weakens the private sector) or as coupons for private distributors (strengthens the private sector).

However, all too strict regulation inhibits entrepreneurial development and institutional and organisational innovation. Financing the wrong (unsustainably operating, not repaying) actors via government credit steering, the undermining of repayment discipline e.g. through politically motivated debt relief, or the introduction of non-cost-covering interest rates can force production chains into inefficiency for several years or even bring about their collapse. This is not just a theoretical danger but a practice which has been frequently observed for decades.

Special attention ought to be given to the aspect that different types of farmers may require very different packages of financial and non-financial technologies, inputs and services. In addition to technical support, the smallest among them in particular need significantly more organisational as well as psychological support (functional and awareness-creating alphabetisation, group forming, etc.). Here, it has to be borne in mind that support needs to change in the course of time, and with the evolution of the clients, the supply chains and the framework conditions.

Michael Brüntrup is an agricultural engineer who did his doctorate on cotton growing in Benin/West Africa. Since 2003, he has worked for what is now the German Institute of Development and Sustainability (IDOS) in Bonn, Germany, and used to be the German Development Institute (DIE), where he generally deals with agricultural policy and food security issues in sub-Saharan Africa. His current research focus is on agro-industry and rural development, drought management and the role of knowledge in agricultural development.

Contact: michael.bruentrup(at)idos-research.de

References:

Adjognon, S. G., Liverpool-Tasie, L. S. O., & Reardon, T. A. (2017). Agricultural input credit in Sub-Saharan Africa: Telling myth from facts. Food policy, 67, 93-105.

Brüntrup, M (2016): Revamping the „Rural Worlds“, Rural 21 50 (2), 16-19.

https://www.rural21.com/fileadmin/downloads/2016/en-02/rural2016_02-S16-19.pdf

Brüntrup, M (2017): Financing agricultural mechanisation, Rural 21.

ttps://www.rural21.com/english/news/detail/article/financing-agricultural-mechanisation.html

Brüntrup, M., Schwarz, F., Absmayr, T., Dylla, J., Eckhard, F., Remke, K., & Sternisko, K. (2018). Nucleus-outgrower schemes as an alternative to traditional smallholder agriculture in Tanzania–strengths, weaknesses and policy requirements. Food Security, 10(4), 807-826.

McKague, K., Jiwa, F., Harji, K., & Ezezika, O. (2021). Scaling social franchises: lessons learned from Farm Shop. Agriculture & Food Security, 10(1), 1-8.

Mukasa, A. N., Simpasa, A. M., & Salami, A. O. (2017). Credit constraints and farm productivity: Micro-level evidence from smallholder farmers in Ethiopia. African Development Bank, (247).

Ströh de Martínez, C., Feddersen, M., & Speicher, A. (2016). Food security in sub-Saharan Africa: a fresh look on agricultural mechanisation. How adapted financial solutions can make a difference, German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE) Studies (No. 91).

ttps://www.idos-research.de/uploads/media/Study_91.pdf

Zander, Rauno (2016): Risks and opportunities of non-bank based financing for agriculture: the case of agricultural value chain financing, German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE) Discussion Paper No. 7/2016.

www.idos-research.de/en/discussion-paper/article/risks-and-opportunities-of-non-bank-based-financing-for-agriculture-the-case-of-agricultural-value-chain-financing/

News Comments

Current Print Issue

Add a comment

Comments :

article and tthe rest of the website is very good. https://Waste-ndc.pro/community/profile/tressa79906983/