An LNG tanker berthed at a terminal to deliver liquid natural gas. Photo: Shutterstock/Wojciech Wrzesien

Global energy flows in transition

The global energy supply is still based very solidly on fossil fuels: natural gas, coal and mineral oil. Traditionally, the bulk of these resources has come from the “strategic energy ellipse”, an area stretching from the Middle East to the Caspian Basin and onwards into Russia’s far north and containing around 70 per cent of the world’s known conventional oil and gas reserves. Most members of the Organization of the Petroleum Exporting Countries (OPEC) are located in this region. Russia, not officially a member of OPEC, has also built up substantial oil and gas export capacities. Over the last two decades, the United States of America (USA) has emerged as one of the leading producers of oil and gas, mainly based on its adoption of fracking technology. The oil crises back in the 1970s led to energy-saving, the development of new technologies, efforts to reduce dependency on fossil fuel imports and, finally, the start of the expansion of renewable energies. As a result of all these factors, OPEC’s significance declined. At the same time, the OPEC members have still managed to secure a substantial share of the market and generate revenue running into billions, not least due to the rise of the People’s Republic of China, now established as a new player – with an ever-increasing demand for energy – on the world’s economic stage.

The established model is in crisis

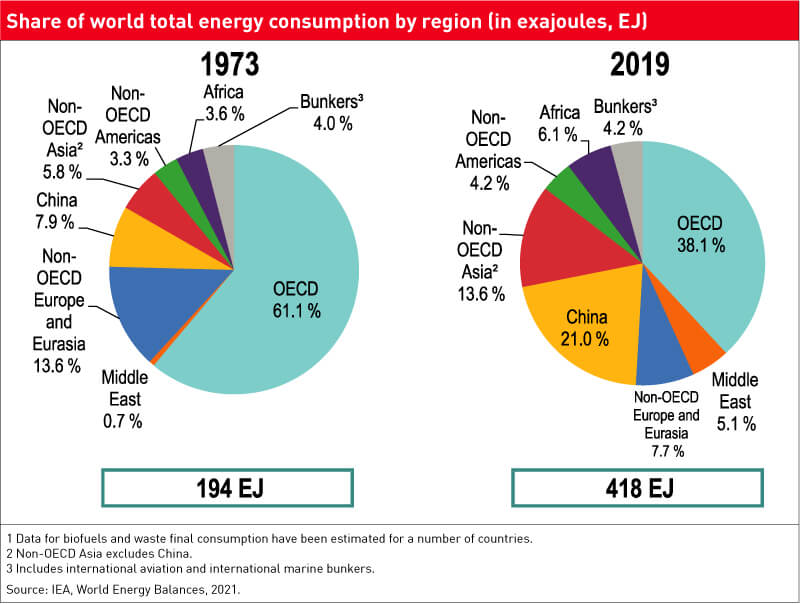

According to figures from the International Energy Agency (IEA), global energy consumption has more than doubled since the early 1970s, rising from 194 to 418 exajoules (EJ). The highly industrialised OECD countries in North America and Europe, but also Japan, are still the largest consumers of energy. However, in these regions, a stagnation or, in some cases, even a decline in primary energy consumption can be observed. The countries in them have made successful efforts, partly through improvements in energy efficiency, to decouple economic growth from energy consumption. This contrasts starkly with the situation in the emerging economies in South and East Asia (mainly China, India, South Korea and Indonesia). In the last four decades, a substantial proportion of global energy consumption has shifted towards these regions (see Figure below). Looking ahead, given its consistently high rate of population growth, over the coming decades, Africa is also set to become a significant factor in the global game of Energy Monopoly.

Fossil fuels – oil, gas and coal – are transported thousands of miles around the world by ship or pipeline before they reach the major hubs in Europe, North America and China where these resources are consumed. According to the IEA, Saudi Arabia, Russia, Iraq, Canada and the United Arab Emirates (UAE) are the world’s largest oil exporters. China, India, the USA, Japan and South Korea are the largest importers in numerical terms. With natural gas, it is a rather different situation. The five largest exporters are Russia, Qatar, Norway, Australia and the USA. The largest gas importers – and heavily dependent on these imports in some cases – are China, Japan, Germany, Italy and Mexico.

Renewables – no longer a privilege of the rich countries

Since around 2000, a highly dynamic expansion of renewable energies (mainly wind and photovoltaics) has also been observed world-wide. According to EurObserv’ER, which monitors developments in this industry, renewable energies are already generating significant and positive socio-economic effects. In 2020 alone, renewable energy use in the 27 European Union States (EU-27) avoided 528 million tonnes of CO2 emissions, substituted for 164.6 Mtoe (million tonnes of oil equivalent) of fossil fuel, saved 35 billion euros in imports, and created and maintained 1.3 million jobs in the renewable energy industry.

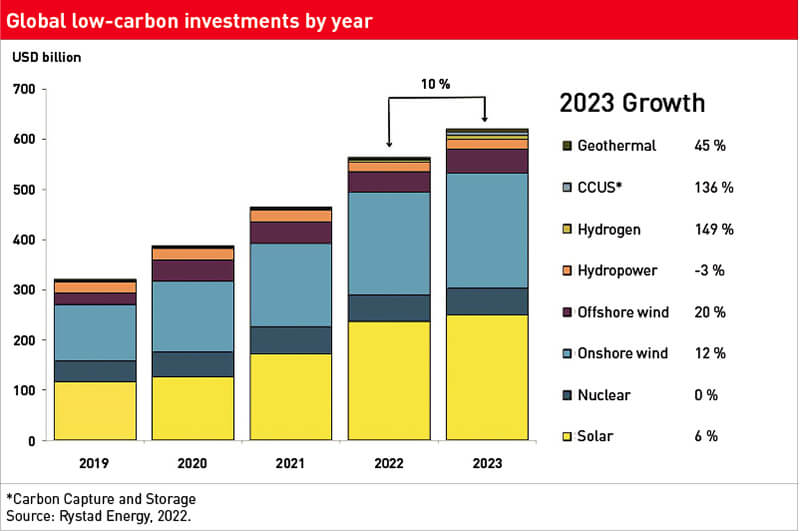

Energy analysts such as Bloomberg New Energy Finance (BNEF) have observed not only a change in trade flows but also noticeable shifts in investment (see Figure below). By far the major share of new investment in the energy sector is now channelled into renewable or low-carbon technologies instead of fossil fuel exploration. According to research by the energy advisory company Rystad Energy, investments in low-carbon energies reached 560 billion US dollars (USD) in 2022; the company is predicting a further rise to 620 billion USD in 2023. Solar and wind (onshore and offshore) will contribute the most by a sizable margin. Alongside hydropower, geothermal and hydrogen, Rystad classes nuclear power, but also carbon capture, utilisation and storage (CCUS), as low-carbon technologies.

Renewable energies, then, are no longer a luxury enjoyed by privileged industrialised countries; they are now a hard economic factor and driver of innovation with commercial viability. Until now, however, renewables have largely been confined to the electricity sector. It is only recently that there has been any development in the electrification of transport – in the form of electric vehicles – and the domestic heat supply, e.g. with heat pumps. Wind, hydropower, solar and geothermal tend, by their very nature, to be available locally. Most of the electricity generated from renewables is fed into the European transmission grids and traded Europe-wide in a liberalised market. Unlike oil, coal and gas, renewables are not traded as a transcontinental commodity: there are no subsea power cables linking Europe with North or South America.

Russia’s war on Ukraine driving global energy transition

For many decades, including the entire duration of the Cold War, Russia was a reliable supplier of affordable gas to Europe. The gas was transported by pipeline through Eastern Europe to the West and was an important pillar of the Western economic and growth model. With Russia’s invasion of Ukraine, this model more or less imploded overnight. In response to Russia’s war of aggression, the European Union (EU) imposed sanctions on Russian companies and individuals from the spheres of politics and business. This has affected the financial, energy and transport sectors. Since then, the EU has been attempting to break free from Russian energy imports as swiftly as possible. At the start of 2021, for example, more than 53 per cent of the gas consumed in Germany came from Russia, but within a matter of months, this had fallen to almost zero, according to figures from the German Association of Energy and Water Industries (BDEW). This was achieved by switching to other gas supplier countries and making significant energy savings in households and industry.

The dramatically accelerated diversification of the energy supply away from Russian gas, which began – not entirely voluntarily – in 2022, does not signify an immediate break with fossil fuel per se. Indeed, in Germany, disused lignite-fired power plants have been brought back into service in order to secure the electricity supply in winter and substitute for natural gas in the energy mix. Several EU countries are turning to the international energy markets to obtain liquefied natural gas (LNG) – which is not entirely free from controversy in terms of its environmental credentials, but is still a highly sought-after commodity. As a result, an LNG supply is now out of reach for the weaker economies. LNG is natural gas that has been cooled to a temperature of -162° Celsius, bringing it to a liquid state in which it occupies only 1/600th of its original volume and allowing it to be transported on tanker ships. These LNG tankers dock at floating terminals, known as Floating Storage and Regasification Units (FSRUs), where the LNG is brought back up to normal temperature and fed into the gas transmission network. The world’s leading LNG exporters include Qatar, Australia and the USA. In the short term, the purpose of the new floating LNG terminals – which have undergone a fast-tracked approval process – is to contribute to energy supply security. In the medium term, the terminal infrastructure should be capable of handling carbon-free hydrogen instead of natural gas. This rapid and comprehensive reduction in the share of Russian gas, oil and coal imports appears to be irreversible, at least for now.

Russia is therefore attempting to compensate for this loss of revenue by redirecting its exports to countries such as China. India, too, is stocking up on cheap crude oil from Russia. However, pending the development and expansion of the necessary pipeline infrastructure, these exports currently amount to no more than a fraction of the previous levels. This has sometimes bizarre and environmentally harmful consequences. As gas wells, once opened, cannot be closed again immediately, Russia often resorts to flaring to burn off the residual natural gas exiting the wells. The Handelsblatt newspaper and other media have also reported on a quite extraordinary situation in which Saudi Arabia – one of the world’s largest petroleum producers – has stocked up on low-cost Russian oil for power generation, thereby benefiting from falling market prices.

New energy sources and new trade flows emerging

Nevertheless, the notion that the heyday of fossil fuels is reaching an end is no longer wishful thinking on the part of environmental NGOs. In its latest World Energy Outlook 2022, the IEA also predicts that the era of fossil fuel growth may soon be over, with global demand for fossil fuels peaking, followed by a steady decline in the coming decades. The kind of energy system required for the future is now a largely uncontentious issue in politics, business and society: what is needed is a radically decarbonised, fossil fuel-free energy system which is substantially reducing its resource consumption and energy-related emissions, if not to zero but certainly to a level compatible with climate neutrality.

Climate neutrality cannot be achieved with the current level of fossil fuel use. The mitigation targets set forth in the Paris Agreement can only be reached if there is a rapid change of direction in many countries’ energy and climate policies, based on carbon-neutral energy use. In recent years, hydrogen has therefore been hailed by many decision-makers as a potential energy source and great hope for the future. Several dozen hydrogen strategies or roadmaps now exist world-wide, and the number of hydrogen projects being announced is steadily increasing. The proclaimed technological and environmental benefits of hydrogen lie in its characteristics as a local carbon-free energy source and its numerous potential applications, including electricity storage and use as a fuel or input in industry and transport.

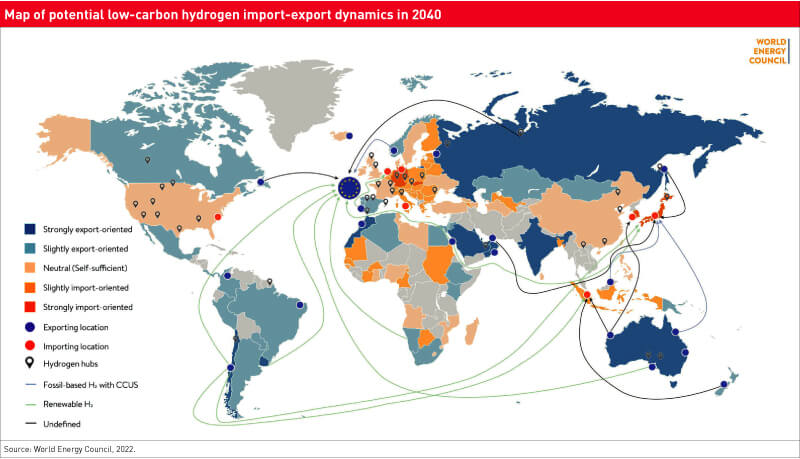

Low-carbon production of hydrogen derivates such as ammonia, methanol and synthetic fuels is theoretically possible. Currently, however, production of hydrogen and its derivates is usually an energy- and therefore emissions-intensive process. The production of renewable hydrogen is most affordable and efficient in the sun-drenched and windswept regions of the world, in theory offering untold economic development opportunities for regions and countries around the world which were never previously thought to have abundant energy resources at their disposal. Indeed, new countries are now appearing on the geopolitical world map and featuring in energy policy debates: alongside the current fossil fuel-exporting countries – Saudi Arabia, Qatar and the UAE, which will have to adapt to a post-fossil world – new actors are positioning themselves with their megaprojects in the prospective hydrogen arena, such as Australia (previously an exporter of coal, now solar power and hydrogen) and Chile (positioning itself as an exporter of hydrogen and silicon as a raw material for batteries and e-mobility). India, South Africa, Morocco, Namibia, Colombia, Mauritania, Oman and Egypt are also moving into position as potential hydrogen producers and exporters – to mention just a few of the countries with new energy and hydrogen ambitions. A “race to hydrogen” can also be observed at present. Through agreements and energy partnerships, the major energy consumers in America, Europe and East Asia are keen to secure access to countries with good climatic conditions for hydrogen production and export.

This creates both opportunities and risks. Becoming an exporter of clean but still rare and therefore valuable renewable hydrogen offers a great development opportunity for previously marginalised economies in the Global South, for it holds out the prospect of growth, employment, prosperity and innovation. At the same time, there is a risk of neocolonial energy extractivism and the “resource curse”, which has afflicted many countries engaged in oil and gas production: the vast export earnings and tax revenue generated by multinational corporations have often ended up in the hands of a small and corrupt elite without significantly improving the living standards of the population at large. Furthermore, it is still unclear which modes of transport for hydrogen will prevail in the medium to long term: hydrogen as a gas, liquefied or in the form of ammonia or methanol, or, alternatively, the use of new storage methods and molecules, known as liquid organic hydrogen carriers (LOHCs). It is likely that several technologies and markets will develop at the global scale, each serving specific applications and industries.

The future energy system will probably be based largely on renewable energy sources and a far higher proportion of temporarily stored energy. But what should this system look like? Should it be centralised or local? How will it be organised (based on market economic principles, or reliant on a high degree of state control and taxation)? How much of a share will accrue to individual energy sources (proportion of renewables, natural gas or nuclear)? Which technologies should – or should not – be utilised to achieve compliance with the Paris climate targets (carbon capture and storage, fracking, geoengineering, or other measures to achieve negative emissions)? Can overall energy and resource consumption be reduced with energy efficiency measures, and if so, how? And what about funding? These pressing energy, climate and technology policy issues are the subject of intense debate in politics, business and society world-wide, and their solutions at the national level will vary widely.

Roman Buss is a political scientist who has been observing the expansion of renewable energies and the hydrogen ramp-up in Germany, Europe and world-wide for many years. He is a Senior Manager at Weltenergierat – Deutschland e.V., the national member representing the Federal Republic of Germany at the World Energy Council, the world’s largest energy body covering all energy resources and technologies.

Contact: buss@weltenergierat.de

References/Further reading:

BDEW 2022, Zahl der Woche LNG: Um 66 Prozent sind die europäischen LNG-Importe im Jahr 2022 im Vergleich zu 2021 gestiegen, BDEW Pressemitteilung vom 13.01.2023,

https://www.bdew.de/presse/presseinformationen/zahl-der-woche-lng-um-66-prozent/

BDEW 2022, Foliensatz zur Publikation „Die Energieversorgung 2022 – Jahresbericht – Bundesverband der Energie- und Wasserwirtschaft e.V. (Hg.), 20.12.2022.

https://www.bdew.de/media/documents/Jahresbericht_2022_Foliensatz_final_20Dez2022.pdf

BNEF 2022, Bloomberg New Energy Finance, Energy Transition Investment Trends 2022,

Energy Transition Investment Trends 2022 | BloombergNEF (bnef.com)

EurObserv’ER 2022, The state of renewable energies in Europe,

https://www.eurobserv-er.org/category/all-annual-overview-barometers/

Handelsblatt 2022, Wie Saudi-Arabien aus den Sanktionen gegen Russland ein Geschäft macht, 14. Juli 2022,

https://www.handelsblatt.com/finanzen/maerkte/devisen-rohstoffe/rohstoffe-wie-saudi-arabien-aus-den-sanktionen-gegen-russland-ein-geschaeft-macht/28508876.html

IEA 2022, Key World Energy Statistics,

https://www.iea.org/reports/key-world-energy-statistics-2021

IEA 2022, World Energy Outlook 2022, Internationale Energieagentur, Paris,

https://www.iea.org/reports/world-energy-outlook-2022

NTV 2023, Kreml hat sich verkalkuliert. Putin hat ein gewaltiges Öl-Problem,

https://www.n-tv.de/wirtschaft/Putin-hat-ein-gewaltiges-Ol-Problem-article23836500.html?utm_source=pocket-newtab-global-de-DE, 11.01.2023

Rystad Energy 2023,Low-carbon investments to rise by $60 billion in 2023 as inflation weakens; hydrogen and CCUS spending to surge,

https://www.rystadenergy.com/news/low-carbon-investments-to-rise-by-60-billion-in-2023-as-inflation-weakens-hydroge

Telepolis 2023, Trotz Sanktionen: USA profitieren weiter von russischen Öllieferungen, 18.01.2023,

https://www.telepolis.de/features/Trotz-Sanktionen-USA-profitieren-weiter-von-russischen-Oellieferungen-7462116.html

Weltenergierat 2022, Energie für Deutschland - Fakten, Perspektiven und Positionen im globalen Kontext,

https://www.weltenergierat.de/publikationen/energie-fuer-deutschland

World Energy Council 2022, World Energy Insights,

https://www.worldenergy.org/assets/downloads/World_Energy_Insights_Executive_Summary_Regional_insights_into_low-carbon_hydrogen_scale_up_April_2022.pdf?v=1653493797, Seiten 5-6

Add a comment

Be the First to Comment