Global food commodity prices will most likely remain elevated for a certain period if energy and fertiliser remain costly and food market supplies are reduced because of additional threats. Photo: Jörg Böthling

Download this article in magazine layout

Download this article in magazine layout

- Share this article

- Subscribe to our newsletter

How global energy and fertiliser markets impact on food security

Global food insecurity reached record highs in 2022. It is a result of many events and developments interacting with one another – including the impacts of the Russian war of aggression against Ukraine, conflicts and droughts in Africa, global climate threats, the corona pandemic and rising prices of energy, fertiliser and food. The interplay of the drivers of energy, fertiliser and food markets is reversing recent trends, making it unlikely to eradicate poverty and reach zero hunger in 2030. According to the World Food Program, the number of people facing acute food insecurity has risen from 135 million to 345 million since 2019. Food price spikes increase social tensions, and may lead to more conflicts and fragile situations in the Global South.Global commodity markets for energy, fertiliser and food are highly correlated. The drivers of these markets cannot be influenced by single decision makers, but thorough assessment may facilitate development of strategies to cope with these shocks and to mitigate social and economic risks.

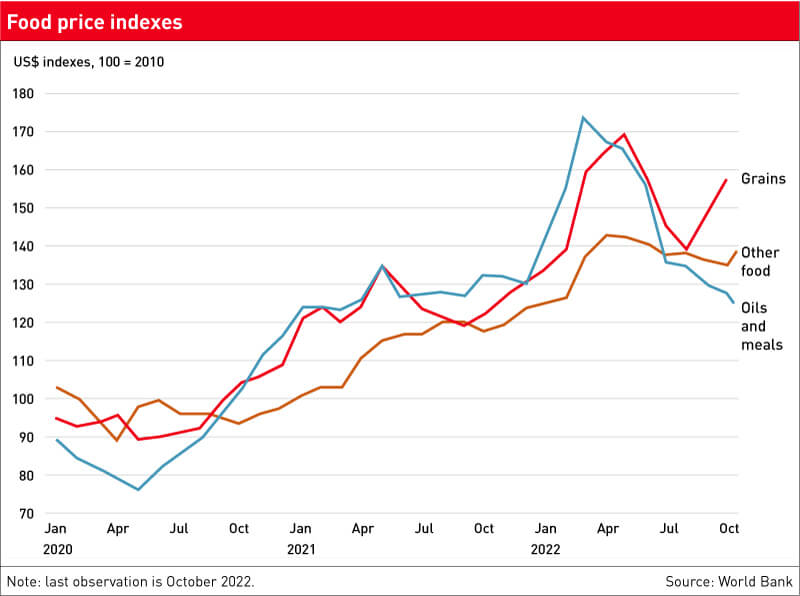

Food prices and fertiliser affordability

Ukraine and Russia provide almost 20 per cent of globally traded cereals; Ukraine supplies more than 50 per cent of globally traded sunflower oil. After the Russian invasion of Ukraine and its blockade of Ukrainian Black Sea ports, food prices reached their peak in April/May 2022 (see Figure below). At the beginning of the war, traders anticipated that Ukraine’s fertiliser, cereals, and oilseeds exports would remain blocked for some time, and Russia’s exports would be constrained by sanctions. As a consequence, prices have almost doubled compared to the previous year. The blockade of Ukrainian Black Sea ports triggered interventions to avoid a global food catastrophe from various international actors from the African Union to the United Nations. Brokered by Turkey’s President Recep Tayyip Erdogan and the UN’s Secretary General António Gutierrez, the Black Sea Grain Initiative was launched, allowing Ukraine to export food commodities under special control mechanisms. Russia’s fertiliser and food exports were not sanctioned. This initiative – and EU countries’ support to ease Ukrainian exports using other routes – had an immediate impact on global cereals and oilseeds markets. As a result, in summer 2022, prices went down by about 10 to 15 per cent. Although Russia threatened to derail this initiative several times through lengthy controls and rocket attacks, the deal has held so far. In the same period, fertiliser prices have also doubled. Various factors, including surging input costs and supply disruptions due to Covid-19, had already caused prices to rise from 2020 to 2021.

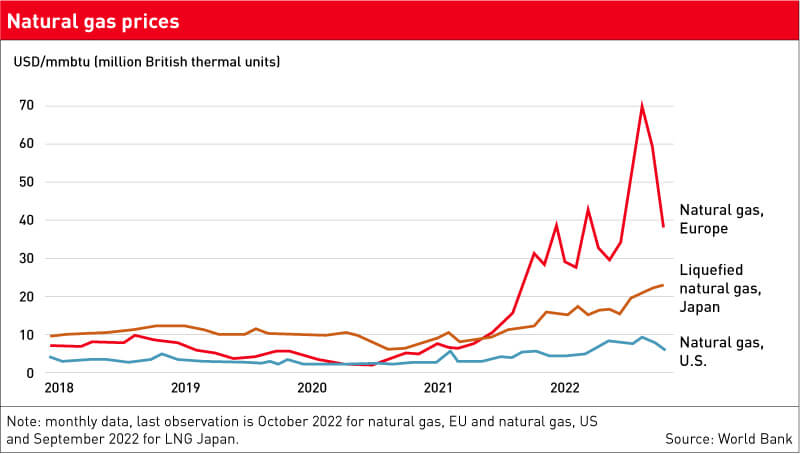

The war in Ukraine amplified supply problems. Russia, Belarus and Ukraine provide about 20 per cent of global nitrogen, potassium and phosphate fertilisers. Nitrogen fertiliser production is very energy-intensive, and rising gas and coal prices (see Figure below) led to widespread production cutbacks. Higher nitrogen prices have also driven up phosphate and potassium prices. Fertiliser prices are expected to stay at historically high levels if gas and coal prices remain elevated. The outlook also depends on the supplies coming from Russia, Ukraine and Belarus to global markets.

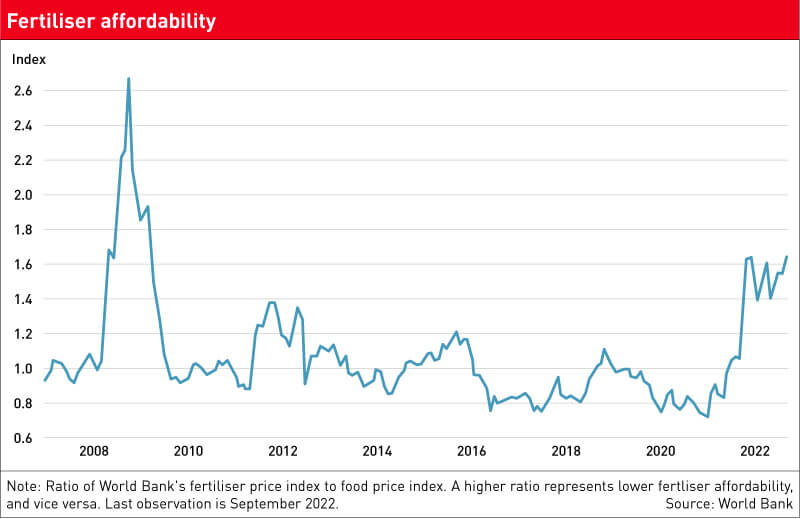

Global cereal and oilseed markets were tight even before the crises, the reason for this being shrinking stocks in 2021 because of fewer supplies from large exporters, including Canada and Russia, and record-high imports from China. Inelastic demand causes a small drop in global harvests to result in cereals and oilseeds prices rising by a large margin. People must eat. That’s why global traders look attentively at monthly international harvest forecasts and the ratio of global stocks and global consumption. If the stock-to-use ratio falls under certain thresholds, food prices react quickly and violently. But if fertiliser prices increase even more than food prices, producers must cut back on input levels they can no longer afford. The World Bank’s fertiliser affordability index measuring the ratio of fertiliser to food prices is at historical high levels and shows this current situation (see Figure below).

Price fluctuations in food and energy markets may further be accelerated by capital markets. If interest rates are low, speculative money is betting on increasing prices at Future Stock Exchanges. Research shows that this significantly amplifies price fluctuations on food markets. Oftentimes, traders of food commodities are not interested in buying or selling the product itself but in realising profits on market trends. Biofuels markets also impact on food commodity markets. The amounts of corn in the USA, rapeseed in Europe and sugar in Brazil that are being transformed into biofuels are huge and impact on food markets. Biofuels demand is very inelastic. Mandates need to be filled at any price. In times of high food prices, biofuels mandates that are set politically should be revisited and if necessary be reduced to lower the pressure on food commodity markets. In times of low prices, the opposite could be done in order to help to reduce food price volatility.

A further known threat to food markets is the weather. The El Niño oscillation in the Pacific is currently in a La Niña phase. Although La Niña has a milder influence on agriculture production than El Niño, it may cause droughts and floods in countries of the Southern Hemisphere, leading to less food production. As climate change is progressing, we may expect more extreme weather conditions leading to droughts and floods adding more risks and volatility to agriculture and food markets.

What must we reckon with?

Higher global food commodity prices will most likely remain elevated for a certain period if energy and fertiliser remain costly and additional threats of climate change, war and conflicts reduce food market supplies. Previous crises suggest a period of about two to three years before higher prices again lead to higher supplies. But this time, it may last longer. With stricter climate action, we may enter a period of longer transition to renewable energy. Expected climate action investments in the energy and fertiliser industries are huge and take time. But even if gas and fertiliser prices do go back to previous levels, food prices may stay elevated. The reason is that the war in Ukraine will continue to reduce supply from the Black Sea region significantly for some years. If Ukraine exports only 20 million tons of cereals annually instead of 50 million tons, food consumers in the world will feel it. To put this into perspective, imagine that one ton of cereals may feed a family of six for a year if based on cereals diets. Thirty million tons less from the Black Sea would thus affect about 180 million people in poor importing countries.

Cereals are particularly important for the poor. Wheat, barley, maize, sorghum and rice account for at least 50 per cent of global nutrition, and as much as 80 per cent in the poorest countries. Global stocks of these crops have been shrinking during the last few years, as demand has outstripped supply. Prices increased sharply from 2020 to 2022. The impact of price spikes on the poor in the Global South is much higher than in industrialised countries for two reasons. First, the share of food in total consumption is much higher. Poor people’s purchasing power goes down, and price increases are felt immediately and violently. Second, the value of public budgets for food security programmes shrinks spectacularly with rising food prices.

Which strategy to choose?

To mitigate the risks of the above triple shock driving inflation and rising costs of capital governments of poor countries must make difficult choices. Budgets are shrinking and need to be invested wisely. Would it make more sense to help consumers in cities to get affordable food, or should this crisis be used to promote producers to increase local production? These are difficult decisions, and solutions will vary from country to country according to priorities, demography, and local production potential. As a rule of thumb, from an economic viewpoint, it is more sensible to help local producers to get affordable seeds, fertilisers, and other inputs than to subsidise products for urban consumers based on imported food commodities. However, policy-makers must also consider social and political consequences – bread prices in cities are highly sensitive to social unrest.

As the area for new farmland is limited in many countries and rules for biodiversity become stricter, more production for growing populations will mainly have to be achieved by climate-smart intensification. Climate-smart agriculture is an approach that helps to transform and reorient agricultural systems to effectively support development and ensure food security in a changing climate. Mitigation of climate change risks can be achieved by reducing carbon emissions by improved farm practices, keeping more organic matter in the soil (carbon sequestration), reducing methane emissions by improved manure management and improved paddy rice cultivation. Adaptation to climate change can be accomplished by fostering resilience for example by developing drought-resistant seed, water-saving technologies and improving land use efficiency. Investments in climate-smart agriculture may offer development and employment opportunities for rural areas.

To avoid confusion, climate-smart doesn’t necessarily mean organic fertiliser only. Sri-Lanka’s recent ill-conceived import ban on mineral fertiliser led to riots and a 30 per cent drop in crop yields forcing the Government to change the policy quickly for good reasons. To feed the world, both organic and mineral fertiliser are necessary. There is simply not enough organic matter available to fully replace mineral fertilisers. In many African countries, governments help farmers to use more fertiliser to increase productivity. Kenya and Rwanda are examples of countries which have increased fertiliser use significantly during the last few years. In future, investments in fertiliser production on the African continent may be considered to ease difficult supply chains and reduce transport costs. It would help to facilitate trade between African countries, which is now lower than with Asia and Europe.

The caveat of fertiliser production, in particular the production of ammonia based on gas, is that it produces a lot of carbon emissions. Ammonia production accounts for around 420 million tonnes of carbon dioxide emissions annually, which together with hydrogen production, responsible for 830 million tons of carbon emissions, create around two per cent of the annual global greenhouse gas emissions. So in future, technology partnerships to produce “green” ammonia and hydrogen will become very important in lowering the climate impact of food value chains.

Higher prices for energy, fertiliser and food create market problems and lead to higher food insecurity, but at the same time present opportunities and incentives to invest in importing countries. Local production gets more competitive. Production of renewable energy, including solar, hydro, wind and bioenergy become more profitable. Incentives to produce organic fertiliser may lead to farmers using more organic matter. Investments in market infrastructure to link local farmers to markets become more attractive. Local food processors may be inclined to replace imported commodities by locally produced agricultural products. Investments in market infrastructure, including transport, storage and processing make importing countries less vulnerable to global shocks.

I would also like to draw attention to solutions to avoid food waste. About one third of global food production is wasted, in industrial countries mainly at the end of the food chain, in households, and in agrarian countries mainly at the beginning of the food chain, on farms. Under tropical conditions in Africa, with bad storage and insufficient transport infrastructure one third of perishable farm produce is rotting away after farmer’s hard work. A transition to off-grid, solar-powered cold storage systems can reduce food waste and make more food available for subsistence and sales, ensuring food security and economic development while minimising the adverse effects of conventional, fossil fuel-based agricultural value chains.

To fend off price hikes and allow food and fertiliser to be supplied to those who need it most, countries need to be encouraged to keep their borders open. Any attempts to constrain exports of food commodities and fertilisers should be avoided. Where possible, trade barriers should be lowered and idle production capacities be used to deliver more food to the world. Joint action helps to keep markets open and prices under control.

Heinz Strubenhoff has worked as a consultant in East Africa and Eastern Europe. For over ten years, Strubenhoff, who holds a PhD in agricultural economics, lived in Ukraine, where he also headed the German-Ukrainian Agricultural Policy Dialogue for Germany’s Federal Ministry of Agriculture and worked for the World Bank’s International Finance Corporation (IFC). He currently lives in Hamburg/Germany, where he is a consultant for KfW and Deutsche Bank.

Contact: hstrubenhoff15@gmail.com

References/Further reading:

https://www.wfp.org/global-hunger-crisis

https://blogs.worldbank.org/opendata/fertilizer-prices-expected-remain-higher-longer

https://thewire.in/economy/speculation-is-contributing-to-global-food-insecurity-significantly

https://blogs.worldbank.org/developmenttalk/risks-global-food-markets

https://www.devex.com/news/time-to-end-the-false-debate-of-organic-vs-mineral-fertiliser-85982

Nigel Poole, Jason Donovan, Olaf Erenstein (2021): Viewpoint: Agri-nutrition research: Revisiting the contribution of maize and wheat to human nutrition and health,Food Policy, Volume 100

Add a comment

Be the First to Comment