Shops closed during the lockdown in Mumbai, India.

Photo: Atul Loke/ NYT/ Redux/ laif

Download this article in magazine layout

Download this article in magazine layout

- Share this article

- Subscribe to our newsletter

Boosting the resilience of the global financial system

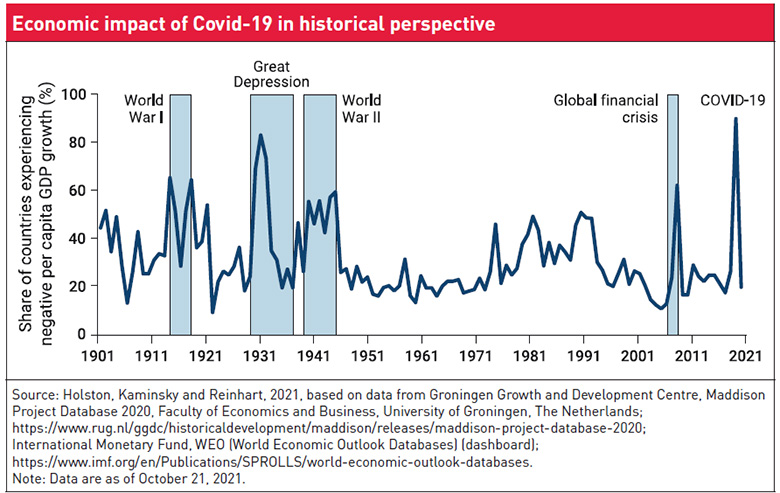

The Covid-19 pandemic triggered the most encompassing economic crisis in almost a century, the recovery from which has been complicated by a war in the heart of Europe. Inflation is rampant, poverty is increasing, and sovereign debt in some countries has reached record levels. These macro-economic signals are clear. Yet under them lie a number of less transparent, hidden risks on the balance sheets of governments and financial institutions that threaten to trigger a tipping point, especially in emerging market and developing economies.

Over 90 per cent of economies saw their gross domestic product fall in 2020. Global growth is projected to drop from 5.7 per cent in 2021 to 2.9 per cent in 2022. In emerging markets and developing economies (EMDEs), growth decreased from 6.6 per cent in 2021 to 3.4 per cent in 2022 – a level much lower than the averages of 4.9 per cent from 2011-2019. Global poverty increased for the first time in a generation, with disproportionate income losses among disadvantaged populations, such as low-income households, women, young adults and workers with lower levels of education.

Crisis response at a high cost

The government-sponsored economic support measures implemented to protect people and businesses from the worst impacts of the pandemic were unprecedented in their size and scale. They included direct payments and debt moratoria for households and businesses, forbearance policies for the financial sector and interest rate measures by Central Banks. Although they blunted the short-term economic impact of the pandemic, they came at a high cost given that many countries had to borrow to fund them. 2020 saw the largest single-year surge in sovereign debt in decades, a remarkable fact given that many low and middle-income governments were already facing record-high debt levels prior to the pandemic. The debt burden of the world’s low-income countries rose 12 per cent to a record 860 billion US dollars (USD), while that of low- and middle-income countries combined climbed 5.3 per cent to 8.7 trillion USD.

The war in Ukraine has further tightened financial conditions globally. According to the recent World Bank Global Economic Prospects report, EMDEs face the tightest financial conditions since the inception of the pandemic. Sovereign spreads have increased – the delta is more significant for commodity importers than exporters. These tightening conditions are showing up in monetary policies, greater volatility and lower risk appetite, which combine to push borrowing costs higher. For low-income countries, the high costs of borrowing could further stall the progress in debt restructuring and could amplify the risk of default on local currency debt. The share of government debt that is non-concessional in the middle- and low-income countries has already risen from less than 60 per cent in 2010 to over 70 per cent today. As fiscal policy continues to tighten over the next couple of years, government debt in 2024 is likely to remain above 2019 levels in over two-thirds of EMDEs. High government debt, in addition to increased debt servicing costs, will limit public investment in social goods and to address development needs.

The pandemic response also stimulated a variety of hidden risks that represent as much of a challenge to the economic recovery as the rising levels of visible sovereign debt. South Asia, for example, is exposed to hidden debt owing to its mounting contingent liabilities. Its increasing leverage of state-owned-enterprises and state-owned commercial banks along with extensive public interventions during the Covid-19 pandemic helped accelerate inclusive economic development. But the region has largely ignored the negative repercussions of mismanagement of risks and inefficiencies. During the pandemic, when most private banks curtailed lending, state-owned commercial banks continued or even increased lending, enabled by capital and debt support from the government. However, evidence suggests that the capital was often misallocated to zombie firms. The war in Ukraine is further magnifying debt distress risks in Central European countries. For example, both the Kyrgyz Republic and Tajikistan are expected to experience output contractions, sharp currency depreciation, and wider fiscal and external current account deficits. Along with the growing cost of borrowing, these record high levels of EMDE debt may trigger a financial crisis similar to the one in the early 1980s.

The risk of hidden debt

We already see signs of unprecedented levels of hidden non-performing loans on the balance sheets of financial institutions across the globe. According to data collected from banks by the International Monetary Fund, non-performing loan rates remained flat between 2019 and 2020 in a sample of advanced and emerging economies that adopted credit forbearance policies. Yet data from businesses tells a different story. Permanent business failures rose nearly 60 per cent in 2020 compared to the pre-pandemic 2019 baseline, according to data on 165 economies from the Mastercard Economics Institute. Roughly 15 per cent of countries, mostly low-and middle-income, continued to see increases in permanent business failure in 2021. And more than 40 per cent of business respondents to the January 2021 World Bank Pulse Enterprise Survey of 24 low- and middle-income countries expected to be in arrears within six months, including over 70 per cent of firms in Nepal and the Philippines and over 60 per cent of firms in Turkey and South Africa.

The inconsistency in reporting between banks and private borrowers lies in the banking moratoria that many countries extended to private debtors during the early stages of the pandemic. Lenders were correspondingly permitted to not reclassify loans in moratoria to a higher risk category, since reclassification would require higher capital provisioning. The idea was that these policies would encourage banks to continue lending despite the pandemic uncertainty. That does not seem to have happened. Lenders in up to 70 per cent of countries began tightening their credit standards in 2020 in response to the first wave of economic pressures brought on by Covid-19. Many maintained tighter conditions throughout 2021, according to Central Bank surveys of bank loan officers. In 2022, European lenders in particular continued to tighten credit standards amidst the persistence of elevated inflation levels and the turbulence and uncertainty stemming from the Russian invasion of Ukraine. The unintended consequence, however, has been to silence the early warning signs of rising loan defaults. Now that supportive government policies have been withdrawn, many vulnerable households and businesses are left with debts they can no longer afford. A possible wave of loan defaults will dampen the already-weak economic recovery, as financial institutions slow lending to stay withing capital provisioning limits. The resulting credit crunch will fall hardest on low-income communities and smaller businesses, exacerbating pre-existing inequalities.

This problem is unlikely to stay contained within the private sector due to the tight interconnections between the balance sheets of households, businesses, financial institutions and governments. A large shock to one sector can generate spillover risks that destabilise the entire economy. For example, if banks end up having insufficient capital to cover the losses from high private loan defaults, governments may be forced to step in to recapitalise them. In this way, private debt transforms into public debt at a time when governments already face heavy debt burdens and strained budgets.

Managing and resolving distressed assets

The proactive recognition and management of distressed assets is an essential first step in addressing the hidden debt crisis to promote continued flow of capital to support the economic recovery and manage the emerging risks of the Russian invasion.

Efforts to re-establish bank portfolio transparency are a critical first step when combined with measures to strengthen capital buffers and improve bank capacity to deal with Non-Performing Loans (NPLs). Countries also need early intervention measures to turn around failing banks in the rare cases when banks are unable to manage the financial stress associated with rising NPLs. These include a legal regime that sets bank failures apart from the country’s general insolvency framework and provides authorities with a wider range of intervention options. The toolkit should also include powers to allocate losses to shareholders and uninsured liability holders, thereby protecting taxpayers against financial sector losses. Private sector-led and -funded solutions should always take priority, leaving public money as a last resort after private sector solutions have been fully exhausted, and only to remedy an acute and demonstrable threat to financial stability.

Effective legal mechanisms to declare bankruptcy or resolve creditor-debtor disputes are another critical policy area to improve economic recovery. Insolvency reforms are associated with wider access to credit, improved creditor recovery, stronger job preservation, higher productivity and lower failure rates among small businesses. Yet many countries, especially low-income countries, lack robust insolvency systems. Cost-reducing reforms can also create the right conditions for nonviable firms to file for liquidation, which will facilitate the flow of credit to more productive parts of the economy.

The government of Serbia, for example, established a national NPL working group in May 2015 after the banking system’s NPL ratio had risen to 23.5 per cent in the aftermath of the global financial crisis. The working group included participants from the public and private sectors to develop and implement a comprehensive strategy for the reduction of NPLs that led to a rapid decline in the NPL ratio to a historic low of 3.4 per cent in September 2020.

Special procedures for micro-, small-, and medium-sized enterprises (MSMEs) are particularly essential for making insolvency mechanisms more accessible. The historic benefits of specialised procedures for MSMEs can be seen in Southeast Asia, which experienced widespread debt distress in the 1980s and 1990s, with NPL rates exceeding 40 per cent in some jurisdictions. In response, the Republic of Korea, Malaysia and Thailand implemented reforms that defined separate procedures for large complex cases and for small firms. Korea reached restructuring agreements for about 80 per cent of registered cases, representing about 95 per cent of corporate debt.

Managing credit risk to encourage lending

Another key area critical to promoting an active recovery lies in improving the ability of banks to assess and manage the risks associated with lending, and thereby mitigate the tendency to limit lending during times of economic uncertainty.

A further consequence of the pandemic and the government debt moratoria and forbearance policies has been to obscure the real economic status of certain households and businesses. In countries where banks weren’t required to report on non-payments of loans subject to moratoria, credit bureau data is both outdated and incomplete, rendering it less effective as a tool for assessing the viability of a prospective borrower. There are also the millions of residents in low-income countries who don’t participate in the formal financial system in a way that allows them to accrue a credit history. In the current environment of economic disruption – which alone tends to make lenders skittish – the lack of risk transparency contributes to widespread credit tightening, especially for higher risk, though viable, borrowers.

New technology-enabled mechanisms to improve risk visibility offers one opportunity. Efforts to integrate “alternative” data into risk calculations shows high promise for achieving a more current risk profile of all customers, including those who lack traditional credit histories. Examples of “alternative” data include utility bills, business receipts and other non-traditional sources that can be used to assess a borrower’s ability to repay a loan. In Germany, researchers found that credit scoring models based on digital footprints were better at predicting creditworthiness than credit bureau scores. Loan data from a large fintech lender in India showed that use of mobile and social footprints can improve risk assessments for individuals with credit scores and be an effective indicator for individuals who lack credit bureau records. Research from South America found similar results from the use of call data records to predict credit repayment outcomes for individuals lacking a credit history. And research from China found that the use of such data to assess the probability of default led to increased credit access for borrowers who otherwise would have remained unbanked.

Another opportunity to improve credit risk transparency and limit the risks of default comes from embedded financing models that leverage technology to collateralise future sales. During the pandemic, the digital MSMEs lending platform Konfio in Mexico used electronic invoicing data and payroll information related to firms on its platform to more than double its monthly loan disbursement. Konfio focused on women business owners, who are less likely to receive traditional credit and more likely to benefit from non-collateral-based lending. Digital payments adoption also accelerated during Covid-19 social distancing restrictions, creating new opportunities to leverage financial technology solutions to lending.

The adoption of technology-enabled credit models – including algorithmic lending – requires regulators, supervisors and policy-makers to play a supportive role by facilitating technology-enabled innovation in a context of updated regulatory rules infrastructure and consumer protection policies.

Managing sovereign debt

The financial consequences of the pandemic and the likely Russian default is falling disproportionately on emerging markets and developing economies, which were already finding it harder to pay their debts before the pandemic, and where pandemic recovery has been mostly disappointing. Almost 50 per cent of the world’s poorest countries eligible for the Debt Service Suspension Initiative that ended in 2021 are either in, or at high risk for, debt distress. About 40 per cent of countries in or at high risk of distress are in sub-Saharan Africa, including countries such as Gambia, Ghana, Kenya, Sierra Leone and Zambia. More risk-averse investors and rising international interest rates will make it more costly for them to attract new financing and service existing debt. According to the World Bank’s International Debt Statistics, total external debt servicing relative to exports roughly doubled from 2010 to 2020 – a period of exceptionally low international interest rates.

The average total debt burden among low- and middle-income countries increased by roughly nine percentage points of gross domestic product (GDP) during the first year of the pandemic, compared with an average annual increase of 1.9 percentage points over the previous decade. Over-indebted governments are unable to pay for public goods such as education and public healthcare, thereby risking poorer human development outcomes and abrupt increases in inequality. Countries in debt distress also have limited capacity to cope with future shocks and may be unable to serve as the lender of last resort to private sector companies in need of public assistance.

The absence of a predictable, orderly and rapid process for sovereign debt restructuring is costly and creates uncertainty. The systemic debt crisis that significantly affected emerging economies in the 1980s illustrates the dire economic and social consequences that arise from delayed policy action: in many countries in Latin America and sub-Saharan Africa, inflation surged, currencies crashed, output collapsed, incomes plummeted, and poverty and inequality increased across regions. The 41 countries that defaulted on their government debt between 1980 and 1985 needed an average of eight years to reach pre-crisis GDP per capita levels. In the 20 countries with the worst output drops, the economic and social fallout from the debt crisis continued for more than a decade.

In countries at high risk of debt distress, proactive debt management can reduce the likelihood of default and free up resources to support economic recovery. That involves either debt re-profiling to push back payments or debt restructuring to decrease liabilities. Pre-emptive restructurings are resolved more quickly than post-default restructuring, leading to shorter exclusion periods from global capital markets and smaller output losses. Once a government is in debt distress, however, the options narrow. One primary tool at this stage is debt restructuring, coupled with a medium-term fiscal and economic reform plan. Restructuring requires prompt recognition of the extent of the problem, coordination with and among creditors, and an understanding by all parties that restructuring is the first step toward debt sustainability – not the last. Swift and deep restructuring agreements allow for a more rapid and sustained recovery, yet the historical track record shows that both countries and creditors resist going fast and cutting deep. Even when countries enter negotiations with creditors, they often require multiple rounds of debt restructuring to emerge from debt distress. Nigeria and Poland, for example, each underwent seven debt restructuring deals before finally resolving their unsustainable debts.

One challenge to comprehensive and proactive sovereign debt management in the current era is the complexity involved in sovereign liabilities. Creditors now include a larger share of commercial and non-traditional lenders, at the same time that off-balance sheet public sector borrowing from state-owned enterprises and special-purpose vehicles has also trended higher. Collectively, these developments reduce transparency and complicate coordination among creditors.

Beyond debt restructuring, governments at risk of or in debt distress must also pursue fiscal consolidation and structural reforms – such as improving government revenue streams and controlling the amount and quality of expenditure – to enhance debt servicing capacity. Greater debt transparency, contractual innovations, and tax policy and administration reforms will help facilitate granular debt management, debt renegotiation and access to capital markets over the longer term.

The crises unfolding now in Sri Lanka and a number of other emerging market economies are a wakeup call for the need to identify risk and act now to boost the resilience of the global financial system. Failure to do so will threaten the already fragile pandemic recovery and stoke even wider global inequality.

Leora Klapper is a Lead Economist in the Finance and Private Sector Research Team of the Development Research Group at the World Bank, Washington DC, USA, and a founder of the Global Findex database, which measures how adults around the world save, borrow, make payments and manage risk. She holds a PhD in Financial Economics from New York University Stern School of Business/USA. Contact: lklapper@worldbank.org

Rita Ramalho is a Lead Economist in the World Bank Chief Economist Office. Previously, she led the Global Indicators Group, which housed data products such as Enterprise Surveys, Women Business and the Law, Enabling the Business of Agriculture, as well as other indicator projects. Rita Ramalho holds a PhD in economics from the Massachusetts Institute of Technology/USA. Contact: RRamalho@ifc.org