Small repair workshops are a typical example of informal nonfarm household enterprises.

Photo: Jörg Böthling

Informal household enterprises in sub-Saharan Africa – livelihoods for rural transformation

Informal nonfarm household enterprises (HEs) are a critical part of rural transformation and poverty reduction. At the household level, they are an income source in the off-season or year-round as the rural agricultural and non-agricultural economies develop. At the level of communities, towns, and cities, they are a vibrant part of the economy, creating economic growth and increased incomes. While the history of economic development suggests that they diminish in importance as agriculture and non-agricultural sectors become increasingly modernised and commercialised and countries reach higher incomes levels, HEs are economically and socially important during key transformation phases.

What are informal nonfarm household enterprises?

According to the International Labour Organization and UN statistical definitions, the informal sector is a group of production units which form part of the household sector as household enterprises or, equivalently, unincorporated enterprises owned by household. Key points in this definition are:

- Size: small-scale, self-employment or under five workers who are either household members or casual employees;

- Usually not registered under national law (often national law excludes these businesses from registration requirements); and

- Lack of separation between household and enterprise assets and finances.

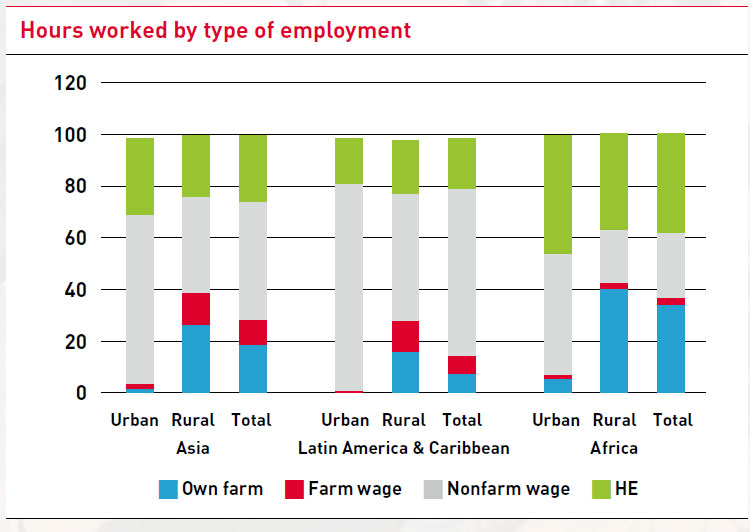

HEs are quite common in rural and urban Africa. In terms of hours worked, HEs account for 40 per cent of total reported hours, more than either wage employment or on-farm activity. In rural areas, they account for as many hours as on-farm work. About 40-50 per cent of rural households have an HE, and for around 40 per cent of rural owners, the HE is their primary livelihood. The majority of HEs are in the retail trade sector, small-scale manufacturing (e.g. oil-seed pressing or furniture making) or service provision (e.g. haircutting or repairs). HEs operate on the street, in a market, or from home. Almost all HEs in Africa sell their goods and services to households or individuals, not to other businesses.

As countries develop, HEs become less common, and wage employment (formal and informal) in modern enterprises more common. In low- and middle-income Asia, HEs account for 26 per cent of reported hours worked, in Latin America for only 20 per cent (see Figure).

Why do they exist?

A range of push and pull factors account for HE existence and growth in rural areas.

- As on-farm incomes rise, household demand increases for a range of nonfarm goods and services which HEs conveniently supply.

- HEs supply services cheaply and conveniently – in the owner’s home, often at off-hours relative to farm work, and in small quantities (e.g. one cigarette), affordable for poorer households with limited cash.

- HEs increase household incomes – by 10 to 60 per cent, depending on the country, sector, scale of operation and location.

- Households have few other opportunities in rural areas to diversify their income sources, as nonfarm wage jobs are scarce and often low-paid.

Even in urban areas in Africa there are not enough wage jobs for those who have the educational and skill qualifications. Currently, African HEs account for as many reported hours worked in urban areas as wage jobs (casual or formal).

Opportunities and constraints

In rural areas, HEs not only offer an opportunity to reduce seasonal underemployment and increase income, they also represent an option to use under-utilised human capital. Outside of a few jobs in the public sector (teachers, health workers or agricultural extension and support), rural Africa offers few opportunities for using secondary education, even as access to this level of education becomes more widespread. In rural HEs, returns to completed primary or some secondary education are high, on average. HEs also offer opportunities for women to have an independent source of income, as these earnings are harder for male family members to appropriate.

Employment in the HE sector in Africa grows almost entirely through household creation of new businesses. Ninety per cent of African HEs have no one outside of family members working in the business. Ninety-five per cent never increase their employment over the life of the business. In other words, these are not growth-oriented enterprise gazelles; that is not the HE business model. While HEs clearly offer opportunities for increased household incomes and consumption, they are nonetheless a precarious livelihood. In both rural and urban areas, HEs depend on other households’ income for demand for their products. This means that any economic shock – a natural disaster, an economic downturn, a global pandemic – hits HE sector incomes hard. In rural communities, they are not immune from the risk agricultural incomes face. Household-specific shocks – such as illness or death – also negatively affect enterprise incomes, even causing business to fail.

HEs tend to be undercapitalised and use limited skills. This makes business entry easy, but also increases competition, pushing down profits. Too small and risky for the formal banking system, HEs are started and survive primarily through loans or gifts from family and friends; some get loans for working capital or new investment from micro-finance institutions (MFIs). HE owners, especially in urban areas, often face harassment, request for bribes, and even assault from suppliers, passers-by or local police. Local governments often ignore them, or worse, slap on punitive taxes or fees (frequently not reported in local accounts), which jeopardises profits and business survival.

Policies to support HE incomes and livelihoods

In the past, economists, urban planners and policy-makers would disparage HEs, often calling them a symptom of failed development policy. In many African countries, this bias continues, especially in larger cities including the capital, as local and national governments seek to establish “world class cities”. In this view, capital cities should have clean, empty sidewalks; no open, covered or night markets so that HEs can sell products, offer services, and prepare and serve food; no small-scale bars created out of shipping containers, no motorcycles, bicycles or rickshaws offering rides; no informal waste picking scavengers, and no unlicensed barbers, haircutters, and manicurists working from home. Advocates of this position want to “clean-up and clean out” the informal sector. They often advocate “formalisation”, a term which has various meanings.

There is no doubt that informal enterprises, if not supported by friendly local governments, can create congestion and hygiene problems. However, efforts to control, reduce or eliminate this sector can impoverish households who own and operate these businesses (or want to open one), as there are simply not enough alternative income-earning opportunities in low- and middle-income countries. Instead, national and local governments could enact policies and programmes to support the survival and growth of this sector, within a national development vision and strategy. Such a development strategy would imply understanding that economic growth and development requires creating more, and more productive, modern labour-intensive enterprises offering good, formal, wage and salary jobs, but until there are enough of these enterprises to employ the majority of the labour force, “informal will be normal”. It would also imply recognising HEs for what they are – and are not.

What would informal-sector-friendly policies look like? Primarily, they would cover:

- The right to exist, and do business in one’s own name, without incorporation.

- Provision of adequate workspaces for different types of businesses within city plans, taking account of HE’s need for electricity, water, sanitation, and solid waste disposal; for market infrastructure to cluster and be near foot traffic (including bus stops and mass transit stations, and in the central business district), and to have a secure place to work and store inventory.

- Financial inclusion, especially cheap and reliable mobile money so that HE owners do not have to carry and store cash (a major business risk) and can record transactions, allowing them to qualify for higher loan amounts or better terms.

- A licensing and permitting regime that is transparent, affordable given HE profit margins, and backed up by reliable public service provision (e.g. police protection in markets).

Some have argued for increased training in business skills for HE owners as well, but these programmes have had almost no success in raising HE profits. Approaches designed to teach negotiation and other “soft skills” appear to have had more success, but the evidence is still meagre, limited to a very few studies.

Some stakeholders argue for “formalising the informal sector”, drawing on evidence that formal businesses (modern, more capital-intensive enterprises) are more productive and pay higher wages. However, this policy prescription misses a key point. If HE owners knew a business model that could be as productive as a modern enterprise employing 20 or more people (and had access to capital to implement it), they would apply it. The informality seen in HEs (small scale, etc.) reflects the only business model which HE owners can implement. They lack the management skills to hire and manage workers, organise production at scale, adopt and adapt new technologies, procure inputs and manage inventory, and develop new customer bases. Asking HE owners to incorporate makes no sense – incorporation offers few benefits, and it would be an increased cost. Incorporation and VAT registration do not change a business model, nor do they make a business more productive or more creditworthy. Informality needs to be permitted for its own sake – as a livelihood strategy.

Louise Fox is an experienced development economist who specialises in strategies for employment creation, opportunity expansion, economic empowerment, and poverty reduction. She is currently Nonresident Senior Fellow, African Growth Initiative, Global Economy and Development, The Brookings Institution, and Visiting Scholar, Blum Center for Developing Economies, University of California, USA.

Contact: fox.louise@outlook.com

Add a comment

Be the First to Comment